- +1 551 333 1547

- +44 2070 979277

- live:skype_chat

Telco Transformation Comprehensive Study by Type (Fixed, Mobile), Application (Retail (Prepaid and Postpaid), Wholesale, Enterprise Consumers), End-Users (Energy, Transport, Healthcare, Government, Entertainment Industry, Residential Consumers, Others) Players and Region - Global Market Outlook to 2027

Telco Transformation Market by XX Submarkets | Forecast Years 2022-2027

Global Telco Transformation Market Overview:

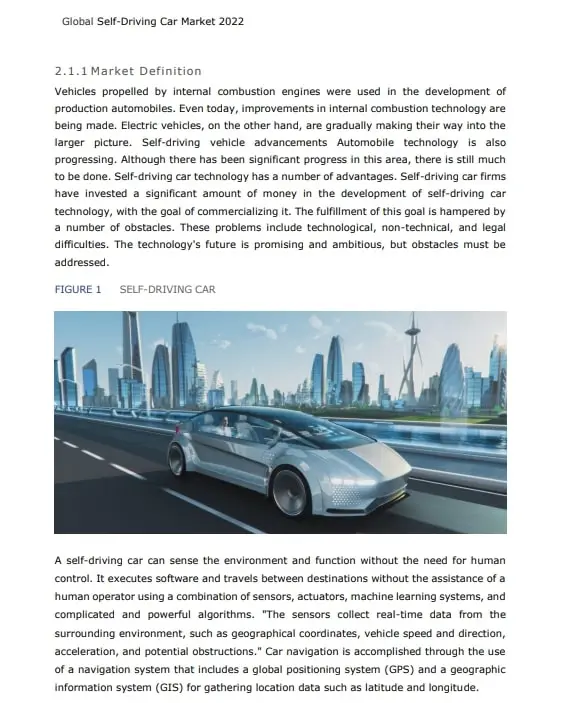

It is the evolution of the telecom industry. The transformation is from the capital-intensive market to the user-centric service model. Some drivers of the transformation are competitive pressure and the disruptive business models of players of the world. To stay in the market and to keep the market going the service providers are providing new attractive services to the end-users which require modifications to the current infrastructure which is typically termed as the next-generation infrastructure. The process of converting and modifying the network elements, end-users, and the business processes so that the competitive advantage offered by the newer generation technology is known as the Transformation.Growth Drivers

- The Decline in Voice Revenues

- Reducing Loyalty and Churn Rate of Subscribers

Roadblocks

- Low Availability of Spectrum

Opportunities

- Emerging New Consumer Segments Such as Banking and Utilities Sector

- Increasing the Network Infrastructure

- Enhancing Data-Based Services

Challenges

- The Emergence of Multiple Technologies

Competitive Landscape:

The companies are exploring the market by adopting mergers & acquisitions, expansions, investments, new service launches, and collaborations as their preferred strategies. The players are exploring new geographies through expansions and acquisitions to avail a competitive advantage through combined synergies.Some of the key players profiled in the report are America Movil Group (United States), AT&T Group (United States), Bharti Airtel Group (India), China Mobile Communications Corp (China), China United Network Communications Group Co., Ltd (China), KPN N.V. (Netherlands), MTN Group (South Africa), Telenor Group (Europe), Deutsche Telekom AG (Germany), NTT Docomo, Inc. (Japan), SK Telecom Co., Ltd. (South Korea), Verizon Wireless (United States), Telefonica, S.A. (Spain), Vivendi SA (France), Vodafone Group Plc (United Kingdom), Alcatel-Lucent (France), LM Ericsson (Sweden), Huawei Technologies Co. Ltd. (China), Nokia Solutions and Networks (Finland) and ZTE Corp (China). Additionally, following companies can also be profiled that are part of our coverage like SoftBank Mobile Corp (Japan), Sprint Corporation (United States), Saudi Telecom Company (Saudi Arabia) and Telecom Italia Group (Italy). Analyst at AMA Research see United States Players to retain maximum share of Global Telco Transformation market by 2027. Considering Market by End-Users, the sub-segment i.e. Energy will boost the Telco Transformation market.

What Can be Explored with the Telco Transformation Market Study

Gain Market Understanding Identify Growth Opportunities

Analyze and Measure the Global Telco Transformation Market by Identifying Investment across various Industry Verticals

Understand the Trends that will drive Future Changes in Telco Transformation

Understand the Competitive Scenario

- Track Right Markets

- Identify the Right Verticals

Research Methodology:

The top-down and bottom-up approaches are used to estimate and validate the size of the Global Telco Transformation market.In order to reach an exhaustive list of functional and relevant players various industry classification standards are closely followed such as NAICS, ICB, SIC to penetrate deep in important geographies by players and a thorough validation test is conducted to reach most relevant players for survey in Telco Transformation market.

In order to make priority list sorting is done based on revenue generated based on latest reporting with the help of paid databases such as Factiva, Bloomberg etc.

Finally the questionnaire is set and specifically designed to address all the necessities for primary data collection after getting prior appointment by targeting key target audience that includes New Entrants/Investors, Analysts and Strategic Business Planners, Providers of Telco Transformation, Venture Capitalists and Private Equity Firms and End-Use Industry.

This helps us to gather the data related to players revenue, operating cycle and expense, profit along with product or service growth etc.

Almost 70-80% of data is collected through primary medium and further validation is done through various secondary sources that includes Regulators, World Bank, Association, Company Website, SEC filings, OTC BB, USPTO, EPO, Annual reports, press releases etc.

Report Objectives / Segmentation Covered

By Type

- Fixed

- Mobile

By Application

- Retail [Prepaid and Postpaid]

- Wholesale

- Enterprise Consumers

By End-Users

- Energy

- Transport

- Healthcare

- Government

- Entertainment Industry

- Residential Consumers

- Others

By Regions

- South America

- Brazil

- Argentina

- Rest of South America

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Australia

- Rest of Asia-Pacific

- Europe

- Germany

- France

- Italy

- United Kingdom

- Netherlands

- Rest of Europe

- MEA

- Middle East

- Africa

- North America

- United States

- Canada

- Mexico

- 1. Market Overview

- 1.1. Introduction

- 1.2. Scope/Objective of the Study

- 1.2.1. Research Objective

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. The Decline in Voice Revenues

- 3.2.2. Reducing Loyalty and Churn Rate of Subscribers

- 3.3. Market Challenges

- 3.3.1. The Emergence of Multiple Technologies

- 3.4. Market Trends

- 3.4.1. A Rise in the Usage of Smartphones

- 3.4.2. The Telecom Industry Is Applying Innovative Technologies Like Artificial Intelligence To Secure Their Network.

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Telco Transformation, by Type, Application, End-Users and Region (value and price ) (2016-2021)

- 5.1. Introduction

- 5.2. Global Telco Transformation (Value)

- 5.2.1. Global Telco Transformation by: Type (Value)

- 5.2.1.1. Fixed

- 5.2.1.2. Mobile

- 5.2.2. Global Telco Transformation by: Application (Value)

- 5.2.2.1. Retail [Prepaid and Postpaid]

- 5.2.2.2. Wholesale

- 5.2.2.3. Enterprise Consumers

- 5.2.3. Global Telco Transformation by: End-Users (Value)

- 5.2.3.1. Energy

- 5.2.3.2. Transport

- 5.2.3.3. Healthcare

- 5.2.3.4. Government

- 5.2.3.5. Entertainment Industry

- 5.2.3.6. Residential Consumers

- 5.2.3.7. Others

- 5.2.4. Global Telco Transformation Region

- 5.2.4.1. South America

- 5.2.4.1.1. Brazil

- 5.2.4.1.2. Argentina

- 5.2.4.1.3. Rest of South America

- 5.2.4.2. Asia Pacific

- 5.2.4.2.1. China

- 5.2.4.2.2. Japan

- 5.2.4.2.3. India

- 5.2.4.2.4. South Korea

- 5.2.4.2.5. Taiwan

- 5.2.4.2.6. Australia

- 5.2.4.2.7. Rest of Asia-Pacific

- 5.2.4.3. Europe

- 5.2.4.3.1. Germany

- 5.2.4.3.2. France

- 5.2.4.3.3. Italy

- 5.2.4.3.4. United Kingdom

- 5.2.4.3.5. Netherlands

- 5.2.4.3.6. Rest of Europe

- 5.2.4.4. MEA

- 5.2.4.4.1. Middle East

- 5.2.4.4.2. Africa

- 5.2.4.5. North America

- 5.2.4.5.1. United States

- 5.2.4.5.2. Canada

- 5.2.4.5.3. Mexico

- 5.2.4.1. South America

- 5.2.1. Global Telco Transformation by: Type (Value)

- 5.3. Global Telco Transformation (Price)

- 5.3.1. Global Telco Transformation by: Type (Price)

- 6. Telco Transformation: Manufacturers/Players Analysis

- 6.1. Competitive Landscape

- 6.1.1. Market Share Analysis

- 6.1.1.1. Top 3

- 6.1.1.2. Top 5

- 6.1.1. Market Share Analysis

- 6.2. Peer Group Analysis (2021)

- 6.3. BCG Matrix

- 6.4. Company Profile

- 6.4.1. America Movil Group (United States)

- 6.4.1.1. Business Overview

- 6.4.1.2. Products/Services Offerings

- 6.4.1.3. Financial Analysis

- 6.4.1.4. SWOT Analysis

- 6.4.2. AT&T Group (United States)

- 6.4.2.1. Business Overview

- 6.4.2.2. Products/Services Offerings

- 6.4.2.3. Financial Analysis

- 6.4.2.4. SWOT Analysis

- 6.4.3. Bharti Airtel Group (India)

- 6.4.3.1. Business Overview

- 6.4.3.2. Products/Services Offerings

- 6.4.3.3. Financial Analysis

- 6.4.3.4. SWOT Analysis

- 6.4.4. China Mobile Communications Corp (China)

- 6.4.4.1. Business Overview

- 6.4.4.2. Products/Services Offerings

- 6.4.4.3. Financial Analysis

- 6.4.4.4. SWOT Analysis

- 6.4.5. China United Network Communications Group Co., Ltd (China)

- 6.4.5.1. Business Overview

- 6.4.5.2. Products/Services Offerings

- 6.4.5.3. Financial Analysis

- 6.4.5.4. SWOT Analysis

- 6.4.6. KPN N.V. (Netherlands)

- 6.4.6.1. Business Overview

- 6.4.6.2. Products/Services Offerings

- 6.4.6.3. Financial Analysis

- 6.4.6.4. SWOT Analysis

- 6.4.7. MTN Group (South Africa)

- 6.4.7.1. Business Overview

- 6.4.7.2. Products/Services Offerings

- 6.4.7.3. Financial Analysis

- 6.4.7.4. SWOT Analysis

- 6.4.8. Telenor Group (Europe)

- 6.4.8.1. Business Overview

- 6.4.8.2. Products/Services Offerings

- 6.4.8.3. Financial Analysis

- 6.4.8.4. SWOT Analysis

- 6.4.9. Deutsche Telekom AG (Germany)

- 6.4.9.1. Business Overview

- 6.4.9.2. Products/Services Offerings

- 6.4.9.3. Financial Analysis

- 6.4.9.4. SWOT Analysis

- 6.4.10. NTT Docomo, Inc. (Japan)

- 6.4.10.1. Business Overview

- 6.4.10.2. Products/Services Offerings

- 6.4.10.3. Financial Analysis

- 6.4.10.4. SWOT Analysis

- 6.4.11. SK Telecom Co., Ltd. (South Korea)

- 6.4.11.1. Business Overview

- 6.4.11.2. Products/Services Offerings

- 6.4.11.3. Financial Analysis

- 6.4.11.4. SWOT Analysis

- 6.4.12. Verizon Wireless (United States)

- 6.4.12.1. Business Overview

- 6.4.12.2. Products/Services Offerings

- 6.4.12.3. Financial Analysis

- 6.4.12.4. SWOT Analysis

- 6.4.13. Telefonica, S.A. (Spain)

- 6.4.13.1. Business Overview

- 6.4.13.2. Products/Services Offerings

- 6.4.13.3. Financial Analysis

- 6.4.13.4. SWOT Analysis

- 6.4.14. Vivendi SA (France)

- 6.4.14.1. Business Overview

- 6.4.14.2. Products/Services Offerings

- 6.4.14.3. Financial Analysis

- 6.4.14.4. SWOT Analysis

- 6.4.15. Vodafone Group Plc (United Kingdom)

- 6.4.15.1. Business Overview

- 6.4.15.2. Products/Services Offerings

- 6.4.15.3. Financial Analysis

- 6.4.15.4. SWOT Analysis

- 6.4.16. Alcatel-Lucent (France)

- 6.4.16.1. Business Overview

- 6.4.16.2. Products/Services Offerings

- 6.4.16.3. Financial Analysis

- 6.4.16.4. SWOT Analysis

- 6.4.17. LM Ericsson (Sweden)

- 6.4.17.1. Business Overview

- 6.4.17.2. Products/Services Offerings

- 6.4.17.3. Financial Analysis

- 6.4.17.4. SWOT Analysis

- 6.4.18. Huawei Technologies Co. Ltd. (China)

- 6.4.18.1. Business Overview

- 6.4.18.2. Products/Services Offerings

- 6.4.18.3. Financial Analysis

- 6.4.18.4. SWOT Analysis

- 6.4.19. Nokia Solutions and Networks (Finland)

- 6.4.19.1. Business Overview

- 6.4.19.2. Products/Services Offerings

- 6.4.19.3. Financial Analysis

- 6.4.19.4. SWOT Analysis

- 6.4.20. ZTE Corp (China)

- 6.4.20.1. Business Overview

- 6.4.20.2. Products/Services Offerings

- 6.4.20.3. Financial Analysis

- 6.4.20.4. SWOT Analysis

- 6.4.1. America Movil Group (United States)

- 6.1. Competitive Landscape

- 7. Global Telco Transformation Sale, by Type, Application, End-Users and Region (value and price ) (2022-2027)

- 7.1. Introduction

- 7.2. Global Telco Transformation (Value)

- 7.2.1. Global Telco Transformation by: Type (Value)

- 7.2.1.1. Fixed

- 7.2.1.2. Mobile

- 7.2.2. Global Telco Transformation by: Application (Value)

- 7.2.2.1. Retail [Prepaid and Postpaid]

- 7.2.2.2. Wholesale

- 7.2.2.3. Enterprise Consumers

- 7.2.3. Global Telco Transformation by: End-Users (Value)

- 7.2.3.1. Energy

- 7.2.3.2. Transport

- 7.2.3.3. Healthcare

- 7.2.3.4. Government

- 7.2.3.5. Entertainment Industry

- 7.2.3.6. Residential Consumers

- 7.2.3.7. Others

- 7.2.4. Global Telco Transformation Region

- 7.2.4.1. South America

- 7.2.4.1.1. Brazil

- 7.2.4.1.2. Argentina

- 7.2.4.1.3. Rest of South America

- 7.2.4.2. Asia Pacific

- 7.2.4.2.1. China

- 7.2.4.2.2. Japan

- 7.2.4.2.3. India

- 7.2.4.2.4. South Korea

- 7.2.4.2.5. Taiwan

- 7.2.4.2.6. Australia

- 7.2.4.2.7. Rest of Asia-Pacific

- 7.2.4.3. Europe

- 7.2.4.3.1. Germany

- 7.2.4.3.2. France

- 7.2.4.3.3. Italy

- 7.2.4.3.4. United Kingdom

- 7.2.4.3.5. Netherlands

- 7.2.4.3.6. Rest of Europe

- 7.2.4.4. MEA

- 7.2.4.4.1. Middle East

- 7.2.4.4.2. Africa

- 7.2.4.5. North America

- 7.2.4.5.1. United States

- 7.2.4.5.2. Canada

- 7.2.4.5.3. Mexico

- 7.2.4.1. South America

- 7.2.1. Global Telco Transformation by: Type (Value)

- 7.3. Global Telco Transformation (Price)

- 7.3.1. Global Telco Transformation by: Type (Price)

- 8. Appendix

- 8.1. Acronyms

- 9. Methodology and Data Source

- 9.1. Methodology/Research Approach

- 9.1.1. Research Programs/Design

- 9.1.2. Market Size Estimation

- 9.1.3. Market Breakdown and Data Triangulation

- 9.2. Data Source

- 9.2.1. Secondary Sources

- 9.2.2. Primary Sources

- 9.3. Disclaimer

- 9.1. Methodology/Research Approach

List of Tables

- Table 1. Telco Transformation: by Type(USD Million)

- Table 2. Telco Transformation Fixed , by Region USD Million (2016-2021)

- Table 3. Telco Transformation Mobile , by Region USD Million (2016-2021)

- Table 4. Telco Transformation: by Application(USD Million)

- Table 5. Telco Transformation Retail [Prepaid and Postpaid] , by Region USD Million (2016-2021)

- Table 6. Telco Transformation Wholesale , by Region USD Million (2016-2021)

- Table 7. Telco Transformation Enterprise Consumers , by Region USD Million (2016-2021)

- Table 8. Telco Transformation: by End-Users(USD Million)

- Table 9. Telco Transformation Energy , by Region USD Million (2016-2021)

- Table 10. Telco Transformation Transport , by Region USD Million (2016-2021)

- Table 11. Telco Transformation Healthcare , by Region USD Million (2016-2021)

- Table 12. Telco Transformation Government , by Region USD Million (2016-2021)

- Table 13. Telco Transformation Entertainment Industry , by Region USD Million (2016-2021)

- Table 14. Telco Transformation Residential Consumers , by Region USD Million (2016-2021)

- Table 15. Telco Transformation Others , by Region USD Million (2016-2021)

- Table 16. South America Telco Transformation, by Country USD Million (2016-2021)

- Table 17. South America Telco Transformation, by Type USD Million (2016-2021)

- Table 18. South America Telco Transformation, by Application USD Million (2016-2021)

- Table 19. South America Telco Transformation, by End-Users USD Million (2016-2021)

- Table 20. Brazil Telco Transformation, by Type USD Million (2016-2021)

- Table 21. Brazil Telco Transformation, by Application USD Million (2016-2021)

- Table 22. Brazil Telco Transformation, by End-Users USD Million (2016-2021)

- Table 23. Argentina Telco Transformation, by Type USD Million (2016-2021)

- Table 24. Argentina Telco Transformation, by Application USD Million (2016-2021)

- Table 25. Argentina Telco Transformation, by End-Users USD Million (2016-2021)

- Table 26. Rest of South America Telco Transformation, by Type USD Million (2016-2021)

- Table 27. Rest of South America Telco Transformation, by Application USD Million (2016-2021)

- Table 28. Rest of South America Telco Transformation, by End-Users USD Million (2016-2021)

- Table 29. Asia Pacific Telco Transformation, by Country USD Million (2016-2021)

- Table 30. Asia Pacific Telco Transformation, by Type USD Million (2016-2021)

- Table 31. Asia Pacific Telco Transformation, by Application USD Million (2016-2021)

- Table 32. Asia Pacific Telco Transformation, by End-Users USD Million (2016-2021)

- Table 33. China Telco Transformation, by Type USD Million (2016-2021)

- Table 34. China Telco Transformation, by Application USD Million (2016-2021)

- Table 35. China Telco Transformation, by End-Users USD Million (2016-2021)

- Table 36. Japan Telco Transformation, by Type USD Million (2016-2021)

- Table 37. Japan Telco Transformation, by Application USD Million (2016-2021)

- Table 38. Japan Telco Transformation, by End-Users USD Million (2016-2021)

- Table 39. India Telco Transformation, by Type USD Million (2016-2021)

- Table 40. India Telco Transformation, by Application USD Million (2016-2021)

- Table 41. India Telco Transformation, by End-Users USD Million (2016-2021)

- Table 42. South Korea Telco Transformation, by Type USD Million (2016-2021)

- Table 43. South Korea Telco Transformation, by Application USD Million (2016-2021)

- Table 44. South Korea Telco Transformation, by End-Users USD Million (2016-2021)

- Table 45. Taiwan Telco Transformation, by Type USD Million (2016-2021)

- Table 46. Taiwan Telco Transformation, by Application USD Million (2016-2021)

- Table 47. Taiwan Telco Transformation, by End-Users USD Million (2016-2021)

- Table 48. Australia Telco Transformation, by Type USD Million (2016-2021)

- Table 49. Australia Telco Transformation, by Application USD Million (2016-2021)

- Table 50. Australia Telco Transformation, by End-Users USD Million (2016-2021)

- Table 51. Rest of Asia-Pacific Telco Transformation, by Type USD Million (2016-2021)

- Table 52. Rest of Asia-Pacific Telco Transformation, by Application USD Million (2016-2021)

- Table 53. Rest of Asia-Pacific Telco Transformation, by End-Users USD Million (2016-2021)

- Table 54. Europe Telco Transformation, by Country USD Million (2016-2021)

- Table 55. Europe Telco Transformation, by Type USD Million (2016-2021)

- Table 56. Europe Telco Transformation, by Application USD Million (2016-2021)

- Table 57. Europe Telco Transformation, by End-Users USD Million (2016-2021)

- Table 58. Germany Telco Transformation, by Type USD Million (2016-2021)

- Table 59. Germany Telco Transformation, by Application USD Million (2016-2021)

- Table 60. Germany Telco Transformation, by End-Users USD Million (2016-2021)

- Table 61. France Telco Transformation, by Type USD Million (2016-2021)

- Table 62. France Telco Transformation, by Application USD Million (2016-2021)

- Table 63. France Telco Transformation, by End-Users USD Million (2016-2021)

- Table 64. Italy Telco Transformation, by Type USD Million (2016-2021)

- Table 65. Italy Telco Transformation, by Application USD Million (2016-2021)

- Table 66. Italy Telco Transformation, by End-Users USD Million (2016-2021)

- Table 67. United Kingdom Telco Transformation, by Type USD Million (2016-2021)

- Table 68. United Kingdom Telco Transformation, by Application USD Million (2016-2021)

- Table 69. United Kingdom Telco Transformation, by End-Users USD Million (2016-2021)

- Table 70. Netherlands Telco Transformation, by Type USD Million (2016-2021)

- Table 71. Netherlands Telco Transformation, by Application USD Million (2016-2021)

- Table 72. Netherlands Telco Transformation, by End-Users USD Million (2016-2021)

- Table 73. Rest of Europe Telco Transformation, by Type USD Million (2016-2021)

- Table 74. Rest of Europe Telco Transformation, by Application USD Million (2016-2021)

- Table 75. Rest of Europe Telco Transformation, by End-Users USD Million (2016-2021)

- Table 76. MEA Telco Transformation, by Country USD Million (2016-2021)

- Table 77. MEA Telco Transformation, by Type USD Million (2016-2021)

- Table 78. MEA Telco Transformation, by Application USD Million (2016-2021)

- Table 79. MEA Telco Transformation, by End-Users USD Million (2016-2021)

- Table 80. Middle East Telco Transformation, by Type USD Million (2016-2021)

- Table 81. Middle East Telco Transformation, by Application USD Million (2016-2021)

- Table 82. Middle East Telco Transformation, by End-Users USD Million (2016-2021)

- Table 83. Africa Telco Transformation, by Type USD Million (2016-2021)

- Table 84. Africa Telco Transformation, by Application USD Million (2016-2021)

- Table 85. Africa Telco Transformation, by End-Users USD Million (2016-2021)

- Table 86. North America Telco Transformation, by Country USD Million (2016-2021)

- Table 87. North America Telco Transformation, by Type USD Million (2016-2021)

- Table 88. North America Telco Transformation, by Application USD Million (2016-2021)

- Table 89. North America Telco Transformation, by End-Users USD Million (2016-2021)

- Table 90. United States Telco Transformation, by Type USD Million (2016-2021)

- Table 91. United States Telco Transformation, by Application USD Million (2016-2021)

- Table 92. United States Telco Transformation, by End-Users USD Million (2016-2021)

- Table 93. Canada Telco Transformation, by Type USD Million (2016-2021)

- Table 94. Canada Telco Transformation, by Application USD Million (2016-2021)

- Table 95. Canada Telco Transformation, by End-Users USD Million (2016-2021)

- Table 96. Mexico Telco Transformation, by Type USD Million (2016-2021)

- Table 97. Mexico Telco Transformation, by Application USD Million (2016-2021)

- Table 98. Mexico Telco Transformation, by End-Users USD Million (2016-2021)

- Table 99. Telco Transformation: by Type(USD/Units)

- Table 100. Company Basic Information, Sales Area and Its Competitors

- Table 101. Company Basic Information, Sales Area and Its Competitors

- Table 102. Company Basic Information, Sales Area and Its Competitors

- Table 103. Company Basic Information, Sales Area and Its Competitors

- Table 104. Company Basic Information, Sales Area and Its Competitors

- Table 105. Company Basic Information, Sales Area and Its Competitors

- Table 106. Company Basic Information, Sales Area and Its Competitors

- Table 107. Company Basic Information, Sales Area and Its Competitors

- Table 108. Company Basic Information, Sales Area and Its Competitors

- Table 109. Company Basic Information, Sales Area and Its Competitors

- Table 110. Company Basic Information, Sales Area and Its Competitors

- Table 111. Company Basic Information, Sales Area and Its Competitors

- Table 112. Company Basic Information, Sales Area and Its Competitors

- Table 113. Company Basic Information, Sales Area and Its Competitors

- Table 114. Company Basic Information, Sales Area and Its Competitors

- Table 115. Company Basic Information, Sales Area and Its Competitors

- Table 116. Company Basic Information, Sales Area and Its Competitors

- Table 117. Company Basic Information, Sales Area and Its Competitors

- Table 118. Company Basic Information, Sales Area and Its Competitors

- Table 119. Company Basic Information, Sales Area and Its Competitors

- Table 120. Telco Transformation: by Type(USD Million)

- Table 121. Telco Transformation Fixed , by Region USD Million (2022-2027)

- Table 122. Telco Transformation Mobile , by Region USD Million (2022-2027)

- Table 123. Telco Transformation: by Application(USD Million)

- Table 124. Telco Transformation Retail [Prepaid and Postpaid] , by Region USD Million (2022-2027)

- Table 125. Telco Transformation Wholesale , by Region USD Million (2022-2027)

- Table 126. Telco Transformation Enterprise Consumers , by Region USD Million (2022-2027)

- Table 127. Telco Transformation: by End-Users(USD Million)

- Table 128. Telco Transformation Energy , by Region USD Million (2022-2027)

- Table 129. Telco Transformation Transport , by Region USD Million (2022-2027)

- Table 130. Telco Transformation Healthcare , by Region USD Million (2022-2027)

- Table 131. Telco Transformation Government , by Region USD Million (2022-2027)

- Table 132. Telco Transformation Entertainment Industry , by Region USD Million (2022-2027)

- Table 133. Telco Transformation Residential Consumers , by Region USD Million (2022-2027)

- Table 134. Telco Transformation Others , by Region USD Million (2022-2027)

- Table 135. South America Telco Transformation, by Country USD Million (2022-2027)

- Table 136. South America Telco Transformation, by Type USD Million (2022-2027)

- Table 137. South America Telco Transformation, by Application USD Million (2022-2027)

- Table 138. South America Telco Transformation, by End-Users USD Million (2022-2027)

- Table 139. Brazil Telco Transformation, by Type USD Million (2022-2027)

- Table 140. Brazil Telco Transformation, by Application USD Million (2022-2027)

- Table 141. Brazil Telco Transformation, by End-Users USD Million (2022-2027)

- Table 142. Argentina Telco Transformation, by Type USD Million (2022-2027)

- Table 143. Argentina Telco Transformation, by Application USD Million (2022-2027)

- Table 144. Argentina Telco Transformation, by End-Users USD Million (2022-2027)

- Table 145. Rest of South America Telco Transformation, by Type USD Million (2022-2027)

- Table 146. Rest of South America Telco Transformation, by Application USD Million (2022-2027)

- Table 147. Rest of South America Telco Transformation, by End-Users USD Million (2022-2027)

- Table 148. Asia Pacific Telco Transformation, by Country USD Million (2022-2027)

- Table 149. Asia Pacific Telco Transformation, by Type USD Million (2022-2027)

- Table 150. Asia Pacific Telco Transformation, by Application USD Million (2022-2027)

- Table 151. Asia Pacific Telco Transformation, by End-Users USD Million (2022-2027)

- Table 152. China Telco Transformation, by Type USD Million (2022-2027)

- Table 153. China Telco Transformation, by Application USD Million (2022-2027)

- Table 154. China Telco Transformation, by End-Users USD Million (2022-2027)

- Table 155. Japan Telco Transformation, by Type USD Million (2022-2027)

- Table 156. Japan Telco Transformation, by Application USD Million (2022-2027)

- Table 157. Japan Telco Transformation, by End-Users USD Million (2022-2027)

- Table 158. India Telco Transformation, by Type USD Million (2022-2027)

- Table 159. India Telco Transformation, by Application USD Million (2022-2027)

- Table 160. India Telco Transformation, by End-Users USD Million (2022-2027)

- Table 161. South Korea Telco Transformation, by Type USD Million (2022-2027)

- Table 162. South Korea Telco Transformation, by Application USD Million (2022-2027)

- Table 163. South Korea Telco Transformation, by End-Users USD Million (2022-2027)

- Table 164. Taiwan Telco Transformation, by Type USD Million (2022-2027)

- Table 165. Taiwan Telco Transformation, by Application USD Million (2022-2027)

- Table 166. Taiwan Telco Transformation, by End-Users USD Million (2022-2027)

- Table 167. Australia Telco Transformation, by Type USD Million (2022-2027)

- Table 168. Australia Telco Transformation, by Application USD Million (2022-2027)

- Table 169. Australia Telco Transformation, by End-Users USD Million (2022-2027)

- Table 170. Rest of Asia-Pacific Telco Transformation, by Type USD Million (2022-2027)

- Table 171. Rest of Asia-Pacific Telco Transformation, by Application USD Million (2022-2027)

- Table 172. Rest of Asia-Pacific Telco Transformation, by End-Users USD Million (2022-2027)

- Table 173. Europe Telco Transformation, by Country USD Million (2022-2027)

- Table 174. Europe Telco Transformation, by Type USD Million (2022-2027)

- Table 175. Europe Telco Transformation, by Application USD Million (2022-2027)

- Table 176. Europe Telco Transformation, by End-Users USD Million (2022-2027)

- Table 177. Germany Telco Transformation, by Type USD Million (2022-2027)

- Table 178. Germany Telco Transformation, by Application USD Million (2022-2027)

- Table 179. Germany Telco Transformation, by End-Users USD Million (2022-2027)

- Table 180. France Telco Transformation, by Type USD Million (2022-2027)

- Table 181. France Telco Transformation, by Application USD Million (2022-2027)

- Table 182. France Telco Transformation, by End-Users USD Million (2022-2027)

- Table 183. Italy Telco Transformation, by Type USD Million (2022-2027)

- Table 184. Italy Telco Transformation, by Application USD Million (2022-2027)

- Table 185. Italy Telco Transformation, by End-Users USD Million (2022-2027)

- Table 186. United Kingdom Telco Transformation, by Type USD Million (2022-2027)

- Table 187. United Kingdom Telco Transformation, by Application USD Million (2022-2027)

- Table 188. United Kingdom Telco Transformation, by End-Users USD Million (2022-2027)

- Table 189. Netherlands Telco Transformation, by Type USD Million (2022-2027)

- Table 190. Netherlands Telco Transformation, by Application USD Million (2022-2027)

- Table 191. Netherlands Telco Transformation, by End-Users USD Million (2022-2027)

- Table 192. Rest of Europe Telco Transformation, by Type USD Million (2022-2027)

- Table 193. Rest of Europe Telco Transformation, by Application USD Million (2022-2027)

- Table 194. Rest of Europe Telco Transformation, by End-Users USD Million (2022-2027)

- Table 195. MEA Telco Transformation, by Country USD Million (2022-2027)

- Table 196. MEA Telco Transformation, by Type USD Million (2022-2027)

- Table 197. MEA Telco Transformation, by Application USD Million (2022-2027)

- Table 198. MEA Telco Transformation, by End-Users USD Million (2022-2027)

- Table 199. Middle East Telco Transformation, by Type USD Million (2022-2027)

- Table 200. Middle East Telco Transformation, by Application USD Million (2022-2027)

- Table 201. Middle East Telco Transformation, by End-Users USD Million (2022-2027)

- Table 202. Africa Telco Transformation, by Type USD Million (2022-2027)

- Table 203. Africa Telco Transformation, by Application USD Million (2022-2027)

- Table 204. Africa Telco Transformation, by End-Users USD Million (2022-2027)

- Table 205. North America Telco Transformation, by Country USD Million (2022-2027)

- Table 206. North America Telco Transformation, by Type USD Million (2022-2027)

- Table 207. North America Telco Transformation, by Application USD Million (2022-2027)

- Table 208. North America Telco Transformation, by End-Users USD Million (2022-2027)

- Table 209. United States Telco Transformation, by Type USD Million (2022-2027)

- Table 210. United States Telco Transformation, by Application USD Million (2022-2027)

- Table 211. United States Telco Transformation, by End-Users USD Million (2022-2027)

- Table 212. Canada Telco Transformation, by Type USD Million (2022-2027)

- Table 213. Canada Telco Transformation, by Application USD Million (2022-2027)

- Table 214. Canada Telco Transformation, by End-Users USD Million (2022-2027)

- Table 215. Mexico Telco Transformation, by Type USD Million (2022-2027)

- Table 216. Mexico Telco Transformation, by Application USD Million (2022-2027)

- Table 217. Mexico Telco Transformation, by End-Users USD Million (2022-2027)

- Table 218. Telco Transformation: by Type(USD/Units)

- Table 219. Research Programs/Design for This Report

- Table 220. Key Data Information from Secondary Sources

- Table 221. Key Data Information from Primary Sources

List of Figures

- Figure 1. Porters Five Forces

- Figure 2. Supply/Value Chain

- Figure 3. PESTEL analysis

- Figure 4. Global Telco Transformation: by Type USD Million (2016-2021)

- Figure 5. Global Telco Transformation: by Application USD Million (2016-2021)

- Figure 6. Global Telco Transformation: by End-Users USD Million (2016-2021)

- Figure 7. South America Telco Transformation Share (%), by Country

- Figure 8. Asia Pacific Telco Transformation Share (%), by Country

- Figure 9. Europe Telco Transformation Share (%), by Country

- Figure 10. MEA Telco Transformation Share (%), by Country

- Figure 11. North America Telco Transformation Share (%), by Country

- Figure 12. Global Telco Transformation: by Type USD/Units (2016-2021)

- Figure 13. Global Telco Transformation share by Players 2021 (%)

- Figure 14. Global Telco Transformation share by Players (Top 3) 2021(%)

- Figure 15. Global Telco Transformation share by Players (Top 5) 2021(%)

- Figure 16. BCG Matrix for key Companies

- Figure 17. America Movil Group (United States) Revenue, Net Income and Gross profit

- Figure 18. America Movil Group (United States) Revenue: by Geography 2021

- Figure 19. AT&T Group (United States) Revenue, Net Income and Gross profit

- Figure 20. AT&T Group (United States) Revenue: by Geography 2021

- Figure 21. Bharti Airtel Group (India) Revenue, Net Income and Gross profit

- Figure 22. Bharti Airtel Group (India) Revenue: by Geography 2021

- Figure 23. China Mobile Communications Corp (China) Revenue, Net Income and Gross profit

- Figure 24. China Mobile Communications Corp (China) Revenue: by Geography 2021

- Figure 25. China United Network Communications Group Co., Ltd (China) Revenue, Net Income and Gross profit

- Figure 26. China United Network Communications Group Co., Ltd (China) Revenue: by Geography 2021

- Figure 27. KPN N.V. (Netherlands) Revenue, Net Income and Gross profit

- Figure 28. KPN N.V. (Netherlands) Revenue: by Geography 2021

- Figure 29. MTN Group (South Africa) Revenue, Net Income and Gross profit

- Figure 30. MTN Group (South Africa) Revenue: by Geography 2021

- Figure 31. Telenor Group (Europe) Revenue, Net Income and Gross profit

- Figure 32. Telenor Group (Europe) Revenue: by Geography 2021

- Figure 33. Deutsche Telekom AG (Germany) Revenue, Net Income and Gross profit

- Figure 34. Deutsche Telekom AG (Germany) Revenue: by Geography 2021

- Figure 35. NTT Docomo, Inc. (Japan) Revenue, Net Income and Gross profit

- Figure 36. NTT Docomo, Inc. (Japan) Revenue: by Geography 2021

- Figure 37. SK Telecom Co., Ltd. (South Korea) Revenue, Net Income and Gross profit

- Figure 38. SK Telecom Co., Ltd. (South Korea) Revenue: by Geography 2021

- Figure 39. Verizon Wireless (United States) Revenue, Net Income and Gross profit

- Figure 40. Verizon Wireless (United States) Revenue: by Geography 2021

- Figure 41. Telefonica, S.A. (Spain) Revenue, Net Income and Gross profit

- Figure 42. Telefonica, S.A. (Spain) Revenue: by Geography 2021

- Figure 43. Vivendi SA (France) Revenue, Net Income and Gross profit

- Figure 44. Vivendi SA (France) Revenue: by Geography 2021

- Figure 45. Vodafone Group Plc (United Kingdom) Revenue, Net Income and Gross profit

- Figure 46. Vodafone Group Plc (United Kingdom) Revenue: by Geography 2021

- Figure 47. Alcatel-Lucent (France) Revenue, Net Income and Gross profit

- Figure 48. Alcatel-Lucent (France) Revenue: by Geography 2021

- Figure 49. LM Ericsson (Sweden) Revenue, Net Income and Gross profit

- Figure 50. LM Ericsson (Sweden) Revenue: by Geography 2021

- Figure 51. Huawei Technologies Co. Ltd. (China) Revenue, Net Income and Gross profit

- Figure 52. Huawei Technologies Co. Ltd. (China) Revenue: by Geography 2021

- Figure 53. Nokia Solutions and Networks (Finland) Revenue, Net Income and Gross profit

- Figure 54. Nokia Solutions and Networks (Finland) Revenue: by Geography 2021

- Figure 55. ZTE Corp (China) Revenue, Net Income and Gross profit

- Figure 56. ZTE Corp (China) Revenue: by Geography 2021

- Figure 57. Global Telco Transformation: by Type USD Million (2022-2027)

- Figure 58. Global Telco Transformation: by Application USD Million (2022-2027)

- Figure 59. Global Telco Transformation: by End-Users USD Million (2022-2027)

- Figure 60. South America Telco Transformation Share (%), by Country

- Figure 61. Asia Pacific Telco Transformation Share (%), by Country

- Figure 62. Europe Telco Transformation Share (%), by Country

- Figure 63. MEA Telco Transformation Share (%), by Country

- Figure 64. North America Telco Transformation Share (%), by Country

- Figure 65. Global Telco Transformation: by Type USD/Units (2022-2027)

List of companies from research coverage that are profiled in the study

- America Movil Group (United States)

- AT&T Group (United States)

- Bharti Airtel Group (India)

- China Mobile Communications Corp (China)

- China United Network Communications Group Co., Ltd (China)

- KPN N.V. (Netherlands)

- MTN Group (South Africa)

- Telenor Group (Europe)

- Deutsche Telekom AG (Germany)

- NTT Docomo, Inc. (Japan)

- SK Telecom Co., Ltd. (South Korea)

- Verizon Wireless (United States)

- Telefonica, S.A. (Spain)

- Vivendi SA (France)

- Vodafone Group Plc (United Kingdom)

- Alcatel-Lucent (France)

- LM Ericsson (Sweden)

- Huawei Technologies Co. Ltd. (China)

- Nokia Solutions and Networks (Finland)

- ZTE Corp (China)

Additional players considered in the study are as follows:

SoftBank Mobile Corp (Japan)

,

Sprint Corporation (United States)

,

Saudi Telecom Company (Saudi Arabia)

,

Telecom Italia Group (Italy)

Select User Access Type

Key Highlights of Report

Apr 2022

227 Pages

68 Tables

Base Year: 2021

Coverage: 15+ Companies; 18 Countries

Request Sample Pages

Budget constraints? Get in touch with us for special pricing

Check Discount Now

Talk to Our Experts

Want to Customize Study?

"We employ Market statistics, Industry benchmarking, Patent analysis, and Technological Insights to derive requirements and provide customize scope of work."

Frequently Asked Questions (FAQ):

The Telco Transformation market is expected to see a CAGR of % during projected year 2021 to 2027.

Top performing companies in the Global Telco Transformation market are America Movil Group (United States), AT&T Group (United States), Bharti Airtel Group (India), China Mobile Communications Corp (China), China United Network Communications Group Co., Ltd (China), KPN N.V. (Netherlands), MTN Group (South Africa), Telenor Group (Europe), Deutsche Telekom AG (Germany), NTT Docomo, Inc. (Japan), SK Telecom Co., Ltd. (South Korea), Verizon Wireless (United States), Telefonica, S.A. (Spain), Vivendi SA (France), Vodafone Group Plc (United Kingdom), Alcatel-Lucent (France), LM Ericsson (Sweden), Huawei Technologies Co. Ltd. (China), Nokia Solutions and Networks (Finland) and ZTE Corp (China), to name a few.

"A Rise in the Usage of Smartphones

" is seen as one of major influencing trends for Telco Transformation Market during projected period 2021-2027.