- +1 551 333 1547

- +44 2070 979277

- live:skype_chat

Automotive Software Comprehensive Study by Type (Dealer Management System, F&I Solution, Electronic Vehicle Registration, Inventory Solutions, Digital Marketing Solution, Others), Application (Manufacturer Retail Store, Automotive Dealer, Automotive Repair Store, Auto Part Wholesaler & Agent), Vehicle Type (Passenger Vehicle, Commercial Vehicles, Electric Vehicle), Software Type (Operating System, Middleware, Application Software) Players and Region - Global Market Outlook to 2028

Automotive Software Market by XX Submarkets | Forecast Years 2023-2028 | CAGR: 12%

Automotive Software Market Scope

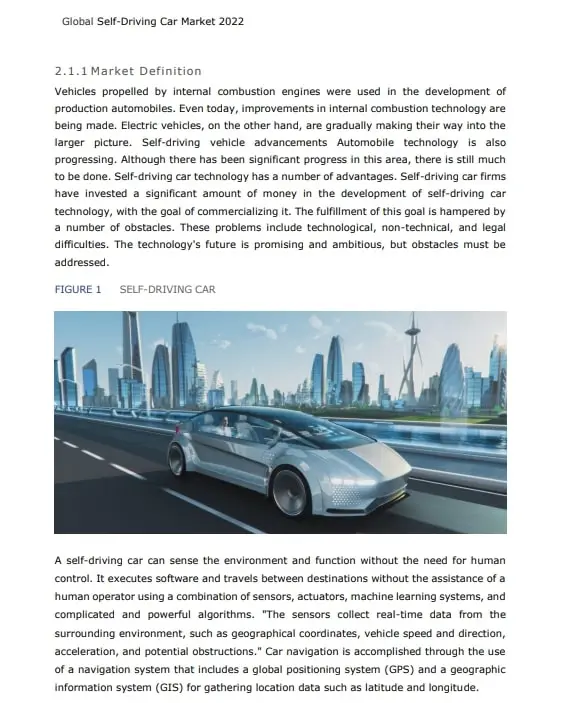

Automotive software is a set of instruction that offers user interact with underlying in-vehicle hardware and also perform control functions in a vehicle. The growing trend of technological advancement, most of the vehicle is equipped with plenty of sensors and software that offers information on various parameters ensuring comfort and safety. In the current scenario, the top players of automotive infotainment systems are shifting towards the PC-like architectural concept, where the functionality of the system is dependent on the central processing unit. The growing popularity of IoV (Internet of Vehicle) and the automotive application gives an edge in market growth. According to AMA, the Global Automotive Software market is expected to see growth rate of 12.0%

Research Analyst at AMA estimates that Chinese, United States Players will contribute to the maximum growth of Global Automotive Software market throughout the predicted period.

CDK Global (United States), Google (United States), Cox Automotive (United States), Reynolds and Reynolds (United States), Dealertrack (United States), Dominion Enterprise (United States), Wipro Limited (India), Infomedia (United States), Epicor (United States), Shoujia Software (China), MAM Software (United Kingdom), Internet Brands (United States), NEC (Japan), Guangzhou Surpass (China) and WHI Solutions (United States) are some of the key players that are part of study coverage. Additionally, the Players which are also part of the research are Yonyou (China), Shenzhen Lianyou (China), Kingdee (China) and Qiming Information (China).

Segmentation Overview

The study have segmented the market of Global Automotive Software market by Type (Dealer Management System, F&I Solution, Electronic Vehicle Registration, Inventory Solutions, Digital Marketing Solution and Others), by Application (Manufacturer Retail Store, Automotive Dealer, Automotive Repair Store and Auto Part Wholesaler & Agent) and Region with country level break-up.On the basis of geography, the market of Automotive Software has been segmented into South America (Brazil, Argentina, Rest of South America), Asia Pacific (China, Japan, India, South Korea, Taiwan, Australia, Rest of Asia-Pacific), Europe (Germany, France, Italy, United Kingdom, Netherlands, Rest of Europe), MEA (Middle East, Africa), North America (United States, Canada, Mexico).

Influencing Trend:

Increasing demand for advance driver assistance system (ADAS), Surging functionality without raising costs and Rising demand for vehicle application such as remote vehicle diagnosticsMarket Growth Drivers:

Technological advancement has led to the incorporation of a number of microprocessors and Product standardization offerings and open-source platformsChallenges:

OEMs are focusing on the development of autonomous vehiclesRestraints:

Lack of autonomous vehicle sells in underdeveloped nationsOpportunities:

Improved circuit analysis and behavioural modelling on a large scale for motors and other major systems and The rise of IoT technology and connected cars, smart mobility and others functionalityMarket Leaders and their Expansionary Development Strategies

In November 2022, MOUNTAIN VIEW, California, and BOULOGNE-BILLANCOURT, France, Renault Group, and Google expanded their partnership with the goal of designing and delivering a digital architecture for the "Software Defined Vehicle" (SDV) and accelerating the group's digitization. The two partners will develop a set of onboard and offboard software components specific to SDV and grow synergies and use cases related to the group's "go to the cloud" strategy.

Automotive software is regulated by the Motor Industry Software Reliability Association (MISRA) standards, as well as ISO 26262 - which is an adaptation of IEC 61508, which governs the functional safety of electronic and programmable electronic safety-related systems.

About Approach

The research aims to propose a patent-based approach in searching for potential technology partners as a supporting tool for enabling open innovation. The study also proposes a systematic searching process of technology partners as a preliminary step to select the emerging and key players that are involved in implementing market estimations. While patent analysis is employed to overcome the aforementioned data- and process-related limitations, as expenses occurred in that technology allows us to estimate the market size by evolving segments as target market from the total available market.

Report Objectives / Segmentation Covered

By Type

- Dealer Management System

- F&I Solution

- Electronic Vehicle Registration

- Inventory Solutions

- Digital Marketing Solution

- Others

By Application

- Manufacturer Retail Store

- Automotive Dealer

- Automotive Repair Store

- Auto Part Wholesaler & Agent

By Vehicle Type

- Passenger Vehicle

- Commercial Vehicles

- Electric Vehicle

By Software Type

- Operating System

- Middleware

- Application Software

By Regions

- South America

- Brazil

- Argentina

- Rest of South America

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Australia

- Rest of Asia-Pacific

- Europe

- Germany

- France

- Italy

- United Kingdom

- Netherlands

- Rest of Europe

- MEA

- Middle East

- Africa

- North America

- United States

- Canada

- Mexico

- 1. Market Overview

- 1.1. Introduction

- 1.2. Scope/Objective of the Study

- 1.2.1. Research Objective

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Technological advancement has led to the incorporation of a number of microprocessors

- 3.2.2. Product standardization offerings and open-source platforms

- 3.3. Market Challenges

- 3.3.1. OEMs are focusing on the development of autonomous vehicles

- 3.4. Market Trends

- 3.4.1. Increasing demand for advance driver assistance system (ADAS)

- 3.4.2. Surging functionality without raising costs

- 3.4.3. Rising demand for vehicle application such as remote vehicle diagnostics

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global Automotive Software, by Type, Application, Vehicle Type, Software Type and Region (value and price ) (2017-2022)

- 5.1. Introduction

- 5.2. Global Automotive Software (Value)

- 5.2.1. Global Automotive Software by: Type (Value)

- 5.2.1.1. Dealer Management System

- 5.2.1.2. F&I Solution

- 5.2.1.3. Electronic Vehicle Registration

- 5.2.1.4. Inventory Solutions

- 5.2.1.5. Digital Marketing Solution

- 5.2.1.6. Others

- 5.2.2. Global Automotive Software by: Application (Value)

- 5.2.2.1. Manufacturer Retail Store

- 5.2.2.2. Automotive Dealer

- 5.2.2.3. Automotive Repair Store

- 5.2.2.4. Auto Part Wholesaler & Agent

- 5.2.3. Global Automotive Software by: Vehicle Type (Value)

- 5.2.3.1. Passenger Vehicle

- 5.2.3.2. Commercial Vehicles

- 5.2.3.3. Electric Vehicle

- 5.2.4. Global Automotive Software by: Software Type (Value)

- 5.2.4.1. Operating System

- 5.2.4.2. Middleware

- 5.2.4.3. Application Software

- 5.2.5. Global Automotive Software Region

- 5.2.5.1. South America

- 5.2.5.1.1. Brazil

- 5.2.5.1.2. Argentina

- 5.2.5.1.3. Rest of South America

- 5.2.5.2. Asia Pacific

- 5.2.5.2.1. China

- 5.2.5.2.2. Japan

- 5.2.5.2.3. India

- 5.2.5.2.4. South Korea

- 5.2.5.2.5. Taiwan

- 5.2.5.2.6. Australia

- 5.2.5.2.7. Rest of Asia-Pacific

- 5.2.5.3. Europe

- 5.2.5.3.1. Germany

- 5.2.5.3.2. France

- 5.2.5.3.3. Italy

- 5.2.5.3.4. United Kingdom

- 5.2.5.3.5. Netherlands

- 5.2.5.3.6. Rest of Europe

- 5.2.5.4. MEA

- 5.2.5.4.1. Middle East

- 5.2.5.4.2. Africa

- 5.2.5.5. North America

- 5.2.5.5.1. United States

- 5.2.5.5.2. Canada

- 5.2.5.5.3. Mexico

- 5.2.5.1. South America

- 5.2.1. Global Automotive Software by: Type (Value)

- 5.3. Global Automotive Software (Price)

- 5.3.1. Global Automotive Software by: Type (Price)

- 6. Automotive Software: Manufacturers/Players Analysis

- 6.1. Competitive Landscape

- 6.1.1. Market Share Analysis

- 6.1.1.1. Top 3

- 6.1.1.2. Top 5

- 6.1.1. Market Share Analysis

- 6.2. Peer Group Analysis (2022)

- 6.3. BCG Matrix

- 6.4. Company Profile

- 6.4.1. CDK Global (United States)

- 6.4.1.1. Business Overview

- 6.4.1.2. Products/Services Offerings

- 6.4.1.3. Financial Analysis

- 6.4.1.4. SWOT Analysis

- 6.4.2. Google (United States)

- 6.4.2.1. Business Overview

- 6.4.2.2. Products/Services Offerings

- 6.4.2.3. Financial Analysis

- 6.4.2.4. SWOT Analysis

- 6.4.3. Cox Automotive (United States)

- 6.4.3.1. Business Overview

- 6.4.3.2. Products/Services Offerings

- 6.4.3.3. Financial Analysis

- 6.4.3.4. SWOT Analysis

- 6.4.4. Reynolds and Reynolds (United States)

- 6.4.4.1. Business Overview

- 6.4.4.2. Products/Services Offerings

- 6.4.4.3. Financial Analysis

- 6.4.4.4. SWOT Analysis

- 6.4.5. Dealertrack (United States)

- 6.4.5.1. Business Overview

- 6.4.5.2. Products/Services Offerings

- 6.4.5.3. Financial Analysis

- 6.4.5.4. SWOT Analysis

- 6.4.6. Dominion Enterprise (United States)

- 6.4.6.1. Business Overview

- 6.4.6.2. Products/Services Offerings

- 6.4.6.3. Financial Analysis

- 6.4.6.4. SWOT Analysis

- 6.4.7. Wipro Limited (India)

- 6.4.7.1. Business Overview

- 6.4.7.2. Products/Services Offerings

- 6.4.7.3. Financial Analysis

- 6.4.7.4. SWOT Analysis

- 6.4.8. Infomedia (United States)

- 6.4.8.1. Business Overview

- 6.4.8.2. Products/Services Offerings

- 6.4.8.3. Financial Analysis

- 6.4.8.4. SWOT Analysis

- 6.4.9. Epicor (United States)

- 6.4.9.1. Business Overview

- 6.4.9.2. Products/Services Offerings

- 6.4.9.3. Financial Analysis

- 6.4.9.4. SWOT Analysis

- 6.4.10. Shoujia Software (China)

- 6.4.10.1. Business Overview

- 6.4.10.2. Products/Services Offerings

- 6.4.10.3. Financial Analysis

- 6.4.10.4. SWOT Analysis

- 6.4.11. MAM Software (United Kingdom)

- 6.4.11.1. Business Overview

- 6.4.11.2. Products/Services Offerings

- 6.4.11.3. Financial Analysis

- 6.4.11.4. SWOT Analysis

- 6.4.12. Internet Brands (United States)

- 6.4.12.1. Business Overview

- 6.4.12.2. Products/Services Offerings

- 6.4.12.3. Financial Analysis

- 6.4.12.4. SWOT Analysis

- 6.4.13. NEC (Japan)

- 6.4.13.1. Business Overview

- 6.4.13.2. Products/Services Offerings

- 6.4.13.3. Financial Analysis

- 6.4.13.4. SWOT Analysis

- 6.4.14. Guangzhou Surpass (China)

- 6.4.14.1. Business Overview

- 6.4.14.2. Products/Services Offerings

- 6.4.14.3. Financial Analysis

- 6.4.14.4. SWOT Analysis

- 6.4.15. WHI Solutions (United States)

- 6.4.15.1. Business Overview

- 6.4.15.2. Products/Services Offerings

- 6.4.15.3. Financial Analysis

- 6.4.15.4. SWOT Analysis

- 6.4.1. CDK Global (United States)

- 6.1. Competitive Landscape

- 7. Global Automotive Software Sale, by Type, Application, Vehicle Type, Software Type and Region (value and price ) (2023-2028)

- 7.1. Introduction

- 7.2. Global Automotive Software (Value)

- 7.2.1. Global Automotive Software by: Type (Value)

- 7.2.1.1. Dealer Management System

- 7.2.1.2. F&I Solution

- 7.2.1.3. Electronic Vehicle Registration

- 7.2.1.4. Inventory Solutions

- 7.2.1.5. Digital Marketing Solution

- 7.2.1.6. Others

- 7.2.2. Global Automotive Software by: Application (Value)

- 7.2.2.1. Manufacturer Retail Store

- 7.2.2.2. Automotive Dealer

- 7.2.2.3. Automotive Repair Store

- 7.2.2.4. Auto Part Wholesaler & Agent

- 7.2.3. Global Automotive Software by: Vehicle Type (Value)

- 7.2.3.1. Passenger Vehicle

- 7.2.3.2. Commercial Vehicles

- 7.2.3.3. Electric Vehicle

- 7.2.4. Global Automotive Software by: Software Type (Value)

- 7.2.4.1. Operating System

- 7.2.4.2. Middleware

- 7.2.4.3. Application Software

- 7.2.5. Global Automotive Software Region

- 7.2.5.1. South America

- 7.2.5.1.1. Brazil

- 7.2.5.1.2. Argentina

- 7.2.5.1.3. Rest of South America

- 7.2.5.2. Asia Pacific

- 7.2.5.2.1. China

- 7.2.5.2.2. Japan

- 7.2.5.2.3. India

- 7.2.5.2.4. South Korea

- 7.2.5.2.5. Taiwan

- 7.2.5.2.6. Australia

- 7.2.5.2.7. Rest of Asia-Pacific

- 7.2.5.3. Europe

- 7.2.5.3.1. Germany

- 7.2.5.3.2. France

- 7.2.5.3.3. Italy

- 7.2.5.3.4. United Kingdom

- 7.2.5.3.5. Netherlands

- 7.2.5.3.6. Rest of Europe

- 7.2.5.4. MEA

- 7.2.5.4.1. Middle East

- 7.2.5.4.2. Africa

- 7.2.5.5. North America

- 7.2.5.5.1. United States

- 7.2.5.5.2. Canada

- 7.2.5.5.3. Mexico

- 7.2.5.1. South America

- 7.2.1. Global Automotive Software by: Type (Value)

- 7.3. Global Automotive Software (Price)

- 7.3.1. Global Automotive Software by: Type (Price)

- 8. Appendix

- 8.1. Acronyms

- 9. Methodology and Data Source

- 9.1. Methodology/Research Approach

- 9.1.1. Research Programs/Design

- 9.1.2. Market Size Estimation

- 9.1.3. Market Breakdown and Data Triangulation

- 9.2. Data Source

- 9.2.1. Secondary Sources

- 9.2.2. Primary Sources

- 9.3. Disclaimer

- 9.1. Methodology/Research Approach

List of Tables

- Table 1. Automotive Software: by Type(USD Billion)

- Table 2. Automotive Software Dealer Management System , by Region USD Billion (2017-2022)

- Table 3. Automotive Software F&I Solution , by Region USD Billion (2017-2022)

- Table 4. Automotive Software Electronic Vehicle Registration , by Region USD Billion (2017-2022)

- Table 5. Automotive Software Inventory Solutions , by Region USD Billion (2017-2022)

- Table 6. Automotive Software Digital Marketing Solution , by Region USD Billion (2017-2022)

- Table 7. Automotive Software Others , by Region USD Billion (2017-2022)

- Table 8. Automotive Software: by Application(USD Billion)

- Table 9. Automotive Software Manufacturer Retail Store , by Region USD Billion (2017-2022)

- Table 10. Automotive Software Automotive Dealer , by Region USD Billion (2017-2022)

- Table 11. Automotive Software Automotive Repair Store , by Region USD Billion (2017-2022)

- Table 12. Automotive Software Auto Part Wholesaler & Agent , by Region USD Billion (2017-2022)

- Table 13. Automotive Software: by Vehicle Type(USD Billion)

- Table 14. Automotive Software Passenger Vehicle , by Region USD Billion (2017-2022)

- Table 15. Automotive Software Commercial Vehicles , by Region USD Billion (2017-2022)

- Table 16. Automotive Software Electric Vehicle , by Region USD Billion (2017-2022)

- Table 17. Automotive Software: by Software Type(USD Billion)

- Table 18. Automotive Software Operating System , by Region USD Billion (2017-2022)

- Table 19. Automotive Software Middleware , by Region USD Billion (2017-2022)

- Table 20. Automotive Software Application Software , by Region USD Billion (2017-2022)

- Table 21. South America Automotive Software, by Country USD Billion (2017-2022)

- Table 22. South America Automotive Software, by Type USD Billion (2017-2022)

- Table 23. South America Automotive Software, by Application USD Billion (2017-2022)

- Table 24. South America Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 25. South America Automotive Software, by Software Type USD Billion (2017-2022)

- Table 26. Brazil Automotive Software, by Type USD Billion (2017-2022)

- Table 27. Brazil Automotive Software, by Application USD Billion (2017-2022)

- Table 28. Brazil Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 29. Brazil Automotive Software, by Software Type USD Billion (2017-2022)

- Table 30. Argentina Automotive Software, by Type USD Billion (2017-2022)

- Table 31. Argentina Automotive Software, by Application USD Billion (2017-2022)

- Table 32. Argentina Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 33. Argentina Automotive Software, by Software Type USD Billion (2017-2022)

- Table 34. Rest of South America Automotive Software, by Type USD Billion (2017-2022)

- Table 35. Rest of South America Automotive Software, by Application USD Billion (2017-2022)

- Table 36. Rest of South America Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 37. Rest of South America Automotive Software, by Software Type USD Billion (2017-2022)

- Table 38. Asia Pacific Automotive Software, by Country USD Billion (2017-2022)

- Table 39. Asia Pacific Automotive Software, by Type USD Billion (2017-2022)

- Table 40. Asia Pacific Automotive Software, by Application USD Billion (2017-2022)

- Table 41. Asia Pacific Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 42. Asia Pacific Automotive Software, by Software Type USD Billion (2017-2022)

- Table 43. China Automotive Software, by Type USD Billion (2017-2022)

- Table 44. China Automotive Software, by Application USD Billion (2017-2022)

- Table 45. China Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 46. China Automotive Software, by Software Type USD Billion (2017-2022)

- Table 47. Japan Automotive Software, by Type USD Billion (2017-2022)

- Table 48. Japan Automotive Software, by Application USD Billion (2017-2022)

- Table 49. Japan Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 50. Japan Automotive Software, by Software Type USD Billion (2017-2022)

- Table 51. India Automotive Software, by Type USD Billion (2017-2022)

- Table 52. India Automotive Software, by Application USD Billion (2017-2022)

- Table 53. India Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 54. India Automotive Software, by Software Type USD Billion (2017-2022)

- Table 55. South Korea Automotive Software, by Type USD Billion (2017-2022)

- Table 56. South Korea Automotive Software, by Application USD Billion (2017-2022)

- Table 57. South Korea Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 58. South Korea Automotive Software, by Software Type USD Billion (2017-2022)

- Table 59. Taiwan Automotive Software, by Type USD Billion (2017-2022)

- Table 60. Taiwan Automotive Software, by Application USD Billion (2017-2022)

- Table 61. Taiwan Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 62. Taiwan Automotive Software, by Software Type USD Billion (2017-2022)

- Table 63. Australia Automotive Software, by Type USD Billion (2017-2022)

- Table 64. Australia Automotive Software, by Application USD Billion (2017-2022)

- Table 65. Australia Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 66. Australia Automotive Software, by Software Type USD Billion (2017-2022)

- Table 67. Rest of Asia-Pacific Automotive Software, by Type USD Billion (2017-2022)

- Table 68. Rest of Asia-Pacific Automotive Software, by Application USD Billion (2017-2022)

- Table 69. Rest of Asia-Pacific Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 70. Rest of Asia-Pacific Automotive Software, by Software Type USD Billion (2017-2022)

- Table 71. Europe Automotive Software, by Country USD Billion (2017-2022)

- Table 72. Europe Automotive Software, by Type USD Billion (2017-2022)

- Table 73. Europe Automotive Software, by Application USD Billion (2017-2022)

- Table 74. Europe Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 75. Europe Automotive Software, by Software Type USD Billion (2017-2022)

- Table 76. Germany Automotive Software, by Type USD Billion (2017-2022)

- Table 77. Germany Automotive Software, by Application USD Billion (2017-2022)

- Table 78. Germany Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 79. Germany Automotive Software, by Software Type USD Billion (2017-2022)

- Table 80. France Automotive Software, by Type USD Billion (2017-2022)

- Table 81. France Automotive Software, by Application USD Billion (2017-2022)

- Table 82. France Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 83. France Automotive Software, by Software Type USD Billion (2017-2022)

- Table 84. Italy Automotive Software, by Type USD Billion (2017-2022)

- Table 85. Italy Automotive Software, by Application USD Billion (2017-2022)

- Table 86. Italy Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 87. Italy Automotive Software, by Software Type USD Billion (2017-2022)

- Table 88. United Kingdom Automotive Software, by Type USD Billion (2017-2022)

- Table 89. United Kingdom Automotive Software, by Application USD Billion (2017-2022)

- Table 90. United Kingdom Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 91. United Kingdom Automotive Software, by Software Type USD Billion (2017-2022)

- Table 92. Netherlands Automotive Software, by Type USD Billion (2017-2022)

- Table 93. Netherlands Automotive Software, by Application USD Billion (2017-2022)

- Table 94. Netherlands Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 95. Netherlands Automotive Software, by Software Type USD Billion (2017-2022)

- Table 96. Rest of Europe Automotive Software, by Type USD Billion (2017-2022)

- Table 97. Rest of Europe Automotive Software, by Application USD Billion (2017-2022)

- Table 98. Rest of Europe Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 99. Rest of Europe Automotive Software, by Software Type USD Billion (2017-2022)

- Table 100. MEA Automotive Software, by Country USD Billion (2017-2022)

- Table 101. MEA Automotive Software, by Type USD Billion (2017-2022)

- Table 102. MEA Automotive Software, by Application USD Billion (2017-2022)

- Table 103. MEA Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 104. MEA Automotive Software, by Software Type USD Billion (2017-2022)

- Table 105. Middle East Automotive Software, by Type USD Billion (2017-2022)

- Table 106. Middle East Automotive Software, by Application USD Billion (2017-2022)

- Table 107. Middle East Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 108. Middle East Automotive Software, by Software Type USD Billion (2017-2022)

- Table 109. Africa Automotive Software, by Type USD Billion (2017-2022)

- Table 110. Africa Automotive Software, by Application USD Billion (2017-2022)

- Table 111. Africa Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 112. Africa Automotive Software, by Software Type USD Billion (2017-2022)

- Table 113. North America Automotive Software, by Country USD Billion (2017-2022)

- Table 114. North America Automotive Software, by Type USD Billion (2017-2022)

- Table 115. North America Automotive Software, by Application USD Billion (2017-2022)

- Table 116. North America Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 117. North America Automotive Software, by Software Type USD Billion (2017-2022)

- Table 118. United States Automotive Software, by Type USD Billion (2017-2022)

- Table 119. United States Automotive Software, by Application USD Billion (2017-2022)

- Table 120. United States Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 121. United States Automotive Software, by Software Type USD Billion (2017-2022)

- Table 122. Canada Automotive Software, by Type USD Billion (2017-2022)

- Table 123. Canada Automotive Software, by Application USD Billion (2017-2022)

- Table 124. Canada Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 125. Canada Automotive Software, by Software Type USD Billion (2017-2022)

- Table 126. Mexico Automotive Software, by Type USD Billion (2017-2022)

- Table 127. Mexico Automotive Software, by Application USD Billion (2017-2022)

- Table 128. Mexico Automotive Software, by Vehicle Type USD Billion (2017-2022)

- Table 129. Mexico Automotive Software, by Software Type USD Billion (2017-2022)

- Table 130. Automotive Software: by Type(USD/Units)

- Table 131. Company Basic Information, Sales Area and Its Competitors

- Table 132. Company Basic Information, Sales Area and Its Competitors

- Table 133. Company Basic Information, Sales Area and Its Competitors

- Table 134. Company Basic Information, Sales Area and Its Competitors

- Table 135. Company Basic Information, Sales Area and Its Competitors

- Table 136. Company Basic Information, Sales Area and Its Competitors

- Table 137. Company Basic Information, Sales Area and Its Competitors

- Table 138. Company Basic Information, Sales Area and Its Competitors

- Table 139. Company Basic Information, Sales Area and Its Competitors

- Table 140. Company Basic Information, Sales Area and Its Competitors

- Table 141. Company Basic Information, Sales Area and Its Competitors

- Table 142. Company Basic Information, Sales Area and Its Competitors

- Table 143. Company Basic Information, Sales Area and Its Competitors

- Table 144. Company Basic Information, Sales Area and Its Competitors

- Table 145. Company Basic Information, Sales Area and Its Competitors

- Table 146. Automotive Software: by Type(USD Billion)

- Table 147. Automotive Software Dealer Management System , by Region USD Billion (2023-2028)

- Table 148. Automotive Software F&I Solution , by Region USD Billion (2023-2028)

- Table 149. Automotive Software Electronic Vehicle Registration , by Region USD Billion (2023-2028)

- Table 150. Automotive Software Inventory Solutions , by Region USD Billion (2023-2028)

- Table 151. Automotive Software Digital Marketing Solution , by Region USD Billion (2023-2028)

- Table 152. Automotive Software Others , by Region USD Billion (2023-2028)

- Table 153. Automotive Software: by Application(USD Billion)

- Table 154. Automotive Software Manufacturer Retail Store , by Region USD Billion (2023-2028)

- Table 155. Automotive Software Automotive Dealer , by Region USD Billion (2023-2028)

- Table 156. Automotive Software Automotive Repair Store , by Region USD Billion (2023-2028)

- Table 157. Automotive Software Auto Part Wholesaler & Agent , by Region USD Billion (2023-2028)

- Table 158. Automotive Software: by Vehicle Type(USD Billion)

- Table 159. Automotive Software Passenger Vehicle , by Region USD Billion (2023-2028)

- Table 160. Automotive Software Commercial Vehicles , by Region USD Billion (2023-2028)

- Table 161. Automotive Software Electric Vehicle , by Region USD Billion (2023-2028)

- Table 162. Automotive Software: by Software Type(USD Billion)

- Table 163. Automotive Software Operating System , by Region USD Billion (2023-2028)

- Table 164. Automotive Software Middleware , by Region USD Billion (2023-2028)

- Table 165. Automotive Software Application Software , by Region USD Billion (2023-2028)

- Table 166. South America Automotive Software, by Country USD Billion (2023-2028)

- Table 167. South America Automotive Software, by Type USD Billion (2023-2028)

- Table 168. South America Automotive Software, by Application USD Billion (2023-2028)

- Table 169. South America Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 170. South America Automotive Software, by Software Type USD Billion (2023-2028)

- Table 171. Brazil Automotive Software, by Type USD Billion (2023-2028)

- Table 172. Brazil Automotive Software, by Application USD Billion (2023-2028)

- Table 173. Brazil Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 174. Brazil Automotive Software, by Software Type USD Billion (2023-2028)

- Table 175. Argentina Automotive Software, by Type USD Billion (2023-2028)

- Table 176. Argentina Automotive Software, by Application USD Billion (2023-2028)

- Table 177. Argentina Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 178. Argentina Automotive Software, by Software Type USD Billion (2023-2028)

- Table 179. Rest of South America Automotive Software, by Type USD Billion (2023-2028)

- Table 180. Rest of South America Automotive Software, by Application USD Billion (2023-2028)

- Table 181. Rest of South America Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 182. Rest of South America Automotive Software, by Software Type USD Billion (2023-2028)

- Table 183. Asia Pacific Automotive Software, by Country USD Billion (2023-2028)

- Table 184. Asia Pacific Automotive Software, by Type USD Billion (2023-2028)

- Table 185. Asia Pacific Automotive Software, by Application USD Billion (2023-2028)

- Table 186. Asia Pacific Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 187. Asia Pacific Automotive Software, by Software Type USD Billion (2023-2028)

- Table 188. China Automotive Software, by Type USD Billion (2023-2028)

- Table 189. China Automotive Software, by Application USD Billion (2023-2028)

- Table 190. China Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 191. China Automotive Software, by Software Type USD Billion (2023-2028)

- Table 192. Japan Automotive Software, by Type USD Billion (2023-2028)

- Table 193. Japan Automotive Software, by Application USD Billion (2023-2028)

- Table 194. Japan Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 195. Japan Automotive Software, by Software Type USD Billion (2023-2028)

- Table 196. India Automotive Software, by Type USD Billion (2023-2028)

- Table 197. India Automotive Software, by Application USD Billion (2023-2028)

- Table 198. India Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 199. India Automotive Software, by Software Type USD Billion (2023-2028)

- Table 200. South Korea Automotive Software, by Type USD Billion (2023-2028)

- Table 201. South Korea Automotive Software, by Application USD Billion (2023-2028)

- Table 202. South Korea Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 203. South Korea Automotive Software, by Software Type USD Billion (2023-2028)

- Table 204. Taiwan Automotive Software, by Type USD Billion (2023-2028)

- Table 205. Taiwan Automotive Software, by Application USD Billion (2023-2028)

- Table 206. Taiwan Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 207. Taiwan Automotive Software, by Software Type USD Billion (2023-2028)

- Table 208. Australia Automotive Software, by Type USD Billion (2023-2028)

- Table 209. Australia Automotive Software, by Application USD Billion (2023-2028)

- Table 210. Australia Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 211. Australia Automotive Software, by Software Type USD Billion (2023-2028)

- Table 212. Rest of Asia-Pacific Automotive Software, by Type USD Billion (2023-2028)

- Table 213. Rest of Asia-Pacific Automotive Software, by Application USD Billion (2023-2028)

- Table 214. Rest of Asia-Pacific Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 215. Rest of Asia-Pacific Automotive Software, by Software Type USD Billion (2023-2028)

- Table 216. Europe Automotive Software, by Country USD Billion (2023-2028)

- Table 217. Europe Automotive Software, by Type USD Billion (2023-2028)

- Table 218. Europe Automotive Software, by Application USD Billion (2023-2028)

- Table 219. Europe Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 220. Europe Automotive Software, by Software Type USD Billion (2023-2028)

- Table 221. Germany Automotive Software, by Type USD Billion (2023-2028)

- Table 222. Germany Automotive Software, by Application USD Billion (2023-2028)

- Table 223. Germany Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 224. Germany Automotive Software, by Software Type USD Billion (2023-2028)

- Table 225. France Automotive Software, by Type USD Billion (2023-2028)

- Table 226. France Automotive Software, by Application USD Billion (2023-2028)

- Table 227. France Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 228. France Automotive Software, by Software Type USD Billion (2023-2028)

- Table 229. Italy Automotive Software, by Type USD Billion (2023-2028)

- Table 230. Italy Automotive Software, by Application USD Billion (2023-2028)

- Table 231. Italy Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 232. Italy Automotive Software, by Software Type USD Billion (2023-2028)

- Table 233. United Kingdom Automotive Software, by Type USD Billion (2023-2028)

- Table 234. United Kingdom Automotive Software, by Application USD Billion (2023-2028)

- Table 235. United Kingdom Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 236. United Kingdom Automotive Software, by Software Type USD Billion (2023-2028)

- Table 237. Netherlands Automotive Software, by Type USD Billion (2023-2028)

- Table 238. Netherlands Automotive Software, by Application USD Billion (2023-2028)

- Table 239. Netherlands Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 240. Netherlands Automotive Software, by Software Type USD Billion (2023-2028)

- Table 241. Rest of Europe Automotive Software, by Type USD Billion (2023-2028)

- Table 242. Rest of Europe Automotive Software, by Application USD Billion (2023-2028)

- Table 243. Rest of Europe Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 244. Rest of Europe Automotive Software, by Software Type USD Billion (2023-2028)

- Table 245. MEA Automotive Software, by Country USD Billion (2023-2028)

- Table 246. MEA Automotive Software, by Type USD Billion (2023-2028)

- Table 247. MEA Automotive Software, by Application USD Billion (2023-2028)

- Table 248. MEA Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 249. MEA Automotive Software, by Software Type USD Billion (2023-2028)

- Table 250. Middle East Automotive Software, by Type USD Billion (2023-2028)

- Table 251. Middle East Automotive Software, by Application USD Billion (2023-2028)

- Table 252. Middle East Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 253. Middle East Automotive Software, by Software Type USD Billion (2023-2028)

- Table 254. Africa Automotive Software, by Type USD Billion (2023-2028)

- Table 255. Africa Automotive Software, by Application USD Billion (2023-2028)

- Table 256. Africa Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 257. Africa Automotive Software, by Software Type USD Billion (2023-2028)

- Table 258. North America Automotive Software, by Country USD Billion (2023-2028)

- Table 259. North America Automotive Software, by Type USD Billion (2023-2028)

- Table 260. North America Automotive Software, by Application USD Billion (2023-2028)

- Table 261. North America Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 262. North America Automotive Software, by Software Type USD Billion (2023-2028)

- Table 263. United States Automotive Software, by Type USD Billion (2023-2028)

- Table 264. United States Automotive Software, by Application USD Billion (2023-2028)

- Table 265. United States Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 266. United States Automotive Software, by Software Type USD Billion (2023-2028)

- Table 267. Canada Automotive Software, by Type USD Billion (2023-2028)

- Table 268. Canada Automotive Software, by Application USD Billion (2023-2028)

- Table 269. Canada Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 270. Canada Automotive Software, by Software Type USD Billion (2023-2028)

- Table 271. Mexico Automotive Software, by Type USD Billion (2023-2028)

- Table 272. Mexico Automotive Software, by Application USD Billion (2023-2028)

- Table 273. Mexico Automotive Software, by Vehicle Type USD Billion (2023-2028)

- Table 274. Mexico Automotive Software, by Software Type USD Billion (2023-2028)

- Table 275. Automotive Software: by Type(USD/Units)

- Table 276. Research Programs/Design for This Report

- Table 277. Key Data Information from Secondary Sources

- Table 278. Key Data Information from Primary Sources

List of Figures

- Figure 1. Porters Five Forces

- Figure 2. Supply/Value Chain

- Figure 3. PESTEL analysis

- Figure 4. Global Automotive Software: by Type USD Billion (2017-2022)

- Figure 5. Global Automotive Software: by Application USD Billion (2017-2022)

- Figure 6. Global Automotive Software: by Vehicle Type USD Billion (2017-2022)

- Figure 7. Global Automotive Software: by Software Type USD Billion (2017-2022)

- Figure 8. South America Automotive Software Share (%), by Country

- Figure 9. Asia Pacific Automotive Software Share (%), by Country

- Figure 10. Europe Automotive Software Share (%), by Country

- Figure 11. MEA Automotive Software Share (%), by Country

- Figure 12. North America Automotive Software Share (%), by Country

- Figure 13. Global Automotive Software: by Type USD/Units (2017-2022)

- Figure 14. Global Automotive Software share by Players 2022 (%)

- Figure 15. Global Automotive Software share by Players (Top 3) 2022(%)

- Figure 16. Global Automotive Software share by Players (Top 5) 2022(%)

- Figure 17. BCG Matrix for key Companies

- Figure 18. CDK Global (United States) Revenue, Net Income and Gross profit

- Figure 19. CDK Global (United States) Revenue: by Geography 2022

- Figure 20. Google (United States) Revenue, Net Income and Gross profit

- Figure 21. Google (United States) Revenue: by Geography 2022

- Figure 22. Cox Automotive (United States) Revenue, Net Income and Gross profit

- Figure 23. Cox Automotive (United States) Revenue: by Geography 2022

- Figure 24. Reynolds and Reynolds (United States) Revenue, Net Income and Gross profit

- Figure 25. Reynolds and Reynolds (United States) Revenue: by Geography 2022

- Figure 26. Dealertrack (United States) Revenue, Net Income and Gross profit

- Figure 27. Dealertrack (United States) Revenue: by Geography 2022

- Figure 28. Dominion Enterprise (United States) Revenue, Net Income and Gross profit

- Figure 29. Dominion Enterprise (United States) Revenue: by Geography 2022

- Figure 30. Wipro Limited (India) Revenue, Net Income and Gross profit

- Figure 31. Wipro Limited (India) Revenue: by Geography 2022

- Figure 32. Infomedia (United States) Revenue, Net Income and Gross profit

- Figure 33. Infomedia (United States) Revenue: by Geography 2022

- Figure 34. Epicor (United States) Revenue, Net Income and Gross profit

- Figure 35. Epicor (United States) Revenue: by Geography 2022

- Figure 36. Shoujia Software (China) Revenue, Net Income and Gross profit

- Figure 37. Shoujia Software (China) Revenue: by Geography 2022

- Figure 38. MAM Software (United Kingdom) Revenue, Net Income and Gross profit

- Figure 39. MAM Software (United Kingdom) Revenue: by Geography 2022

- Figure 40. Internet Brands (United States) Revenue, Net Income and Gross profit

- Figure 41. Internet Brands (United States) Revenue: by Geography 2022

- Figure 42. NEC (Japan) Revenue, Net Income and Gross profit

- Figure 43. NEC (Japan) Revenue: by Geography 2022

- Figure 44. Guangzhou Surpass (China) Revenue, Net Income and Gross profit

- Figure 45. Guangzhou Surpass (China) Revenue: by Geography 2022

- Figure 46. WHI Solutions (United States) Revenue, Net Income and Gross profit

- Figure 47. WHI Solutions (United States) Revenue: by Geography 2022

- Figure 48. Global Automotive Software: by Type USD Billion (2023-2028)

- Figure 49. Global Automotive Software: by Application USD Billion (2023-2028)

- Figure 50. Global Automotive Software: by Vehicle Type USD Billion (2023-2028)

- Figure 51. Global Automotive Software: by Software Type USD Billion (2023-2028)

- Figure 52. South America Automotive Software Share (%), by Country

- Figure 53. Asia Pacific Automotive Software Share (%), by Country

- Figure 54. Europe Automotive Software Share (%), by Country

- Figure 55. MEA Automotive Software Share (%), by Country

- Figure 56. North America Automotive Software Share (%), by Country

- Figure 57. Global Automotive Software: by Type USD/Units (2023-2028)

List of companies from research coverage that are profiled in the study

- CDK Global (United States)

- Google (United States)

- Cox Automotive (United States)

- Reynolds and Reynolds (United States)

- Dealertrack (United States)

- Dominion Enterprise (United States)

- Wipro Limited (India)

- Infomedia (United States)

- Epicor (United States)

- Shoujia Software (China)

- MAM Software (United Kingdom)

- Internet Brands (United States)

- NEC (Japan)

- Guangzhou Surpass (China)

- WHI Solutions (United States)

Additional players considered in the study are as follows:

Yonyou (China)

,

Shenzhen Lianyou (China)

,

Kingdee (China)

,

Qiming Information (China)

Select User Access Type

Key Highlights of Report

May 2023

206 Pages

93 Tables

Base Year: 2022

Coverage: 15+ Companies; 18 Countries

Request Sample Pages

Budget constraints? Get in touch with us for special pricing

Check Discount Now

Talk to Our Experts

Want to Customize Study?

"We employ Market statistics, Industry benchmarking, Patent analysis, and Technological Insights to derive requirements and provide customize scope of work."

Frequently Asked Questions (FAQ):

The Automotive Software study can be customized to meet your requirements. The market size breakdown by type, by end-use application.

The Automotive Software Market is gaining popularity and expected to see strong valuation by 2028 and may reach USD 50.62 Billion .

According to AMA, the Global Automotive Software market is expected to see growth rate of xx%.

The Automotive Software market study includes a random mix of players, including both market leaders and some top growing emerging players. Connect with our sales executive to get a complete of companies available in our research coverage.