- +1 551 333 1547

- +44 2070 979277

- live:skype_chat

eSignature and Certifications Comprehensive Study by Type (Simple electronic signature (SES), Advanced electronic signature (AES), Qualified electronic signature (QES)), Industry Vertical (BFSI, Government & Defence, Real Estate, Healthcare & Life Sciences, Education, Legal, Others), Deployment (On-Premises, Cloud), Organisation Size (Small, Medium, Large) Players and Region - Global Market Outlook to 2027

eSignature and Certifications Market by XX Submarkets | Forecast Years 2022-2027

Global eSignature and Certifications Market Overview:

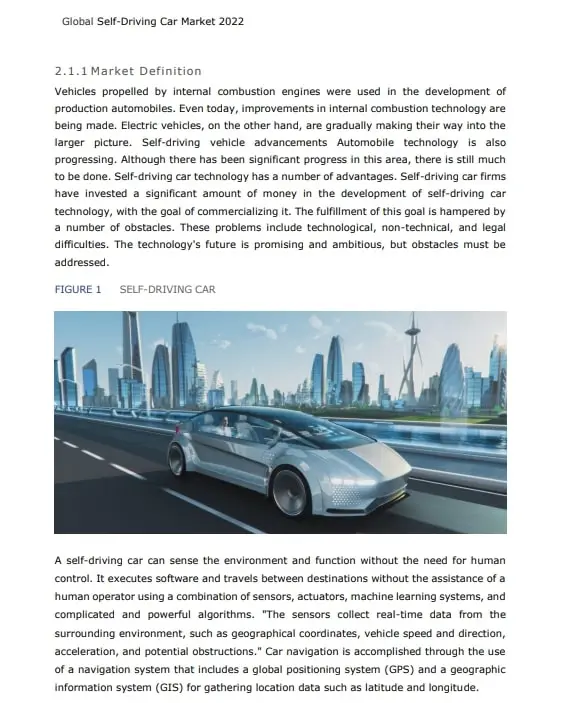

An electronic signature (e-signature) is the digital equivalent of a traditional pen and ink signature. Electronic signatures have the same legal obligations as handwritten signatures, provided they meet the standards. Digital certificates are used to identify the owner of a certificate, securely exchange information with other people and institutions, and electronically sign transmitted data to verify its integrity and provenance. The factors that drive the market are Fast growth in investments in electronic documents by governments and enterprises, upgrades in end-to-end customer experience, and enhanced security with a controlled and seamless workflow.| Attributes | Details |

|---|---|

| Study Period | 2017-2027 |

| Base Year | 2021 |

| Forecast Period | 2022-2027 |

| Historical Period | 2017-2021 |

| Unit | Value (USD Million) |

| Customization Scope | Avail customization with purchase of this report. Add or modify country, region & or narrow down segments in the final scope subject to feasibility |

Influencing Trend:

The growing number of connected devices, including smartphones, tablets, and laptop and Increasing E-Commerce Market Boosting the Growth of eSignatureMarket Growth Drivers:

Fast growth in investments in electronic documents by governments and enterprises, Upgrade in end-to-end customer experience, Enhanced security with a controlled and seamless workflow and Improved operational efficiency at lower OPEXChallenges:

Intensely entrenched traditional business practices and Cost of implementation and legality issuesRestraints:

Lack of awareness about the legality of eSignatures and Variation in eSignature rules and regulations across regionsOpportunities:

Enhancement in the acceptance of cloud-based security solutions, The growing number of partnerships and acquisitions and The rise in artificial intelligenceCompetitive Landscape:

Global eSignature and Certifications is a fragmented market due to the presence of various players. The players are focusing on planning strategic activities like partnerships, mergers, and acquisitions which will help them to sustain in the market and maintain their competitive edge.Some of the key players profiled in the report are SignNow (United States), Aspose Pty Ltd (Australia), ContractSafe (United States), DocuSign (United States), Foxit Software Incorporated (United States), MSB (Sweden), Odoo (United States), OneSpan Sign (United States), Skribble (Switzerland), LULU Software Limited (Canada), Zoho Sign (India) and Rpost (United States). Considering Market by Industry Vertical, the sub-segment i.e. BFSI will boost the eSignature and Certifications market. Considering Market by Deployment, the sub-segment i.e. On-Premises will boost the eSignature and Certifications market. Considering Market by Organisation Size, the sub-segment i.e. Small will boost the eSignature and Certifications market.

Latest Market Insights:

In October 2021, Foxit acquired eSignature Software Leader, eSign Genie. Foxit launched Foxit eSign, a best of breed eSignature service that provides a full, legally binding and secure electronic signature workflow for digital preparation, sharing, signing and collecting of important documents.In September 2022, The UK Legalisation Office will be able to receive documents digitally. It will issue electronic �e-Apostille� certificates enabling a quicker, cheaper, and more efficient service for thousands of people around the globe. A legalized document is needed in many international transactions including overseas working visas and managing property. Currently, customers send their physical documents to the UK Legalisation Office by post or courier and receive the documents back several days later with a paper certificate, known as an Apostille, attached. The first UK e-Apostille was issued on 15 December 2021 as a pilot initiative. The option to apply for an e-Apostille will now be opened up to more customers.

In May 2022, the Moldovan Parliament voted on the new Law on Electronic Identification and Trust Services ("Law 124/2022"). Law 124/2022 will enter into force on 10 December 2022 and replaces the currently existing Law on Electronic Signature and Electronic Document ("Law 91/2014"). This replacement seeks to align the national legislation in the field of electronic signature with European norms, namely the harmonization with Regulation (EU) No 910/2014 of the European Parliament and of the Council of 23 July 2014 on electronic identification and trust services for electronic transactions in the internal market and repealing Directive 1999/93/EC.

What Can be Explored with the eSignature and Certifications Market Study

Gain Market Understanding Identify Growth Opportunities

Analyze and Measure the Global eSignature and Certifications Market by Identifying Investment across various Industry Verticals

Understand the Trends that will drive Future Changes in eSignature and Certifications

Understand the Competitive Scenario

- Track Right Markets

- Identify the Right Verticals

Research Methodology:

The top-down and bottom-up approaches are used to estimate and validate the size of the Global eSignature and Certifications market.In order to reach an exhaustive list of functional and relevant players various industry classification standards are closely followed such as NAICS, ICB, SIC to penetrate deep in important geographies by players and a thorough validation test is conducted to reach most relevant players for survey in eSignature and Certifications market.

In order to make priority list sorting is done based on revenue generated based on latest reporting with the help of paid databases such as Factiva, Bloomberg etc.

Finally the questionnaire is set and specifically designed to address all the necessities for primary data collection after getting prior appointment by targeting key target audience that includes eSignature and Certifications Developers, Regulatory Bodies, Potential Investors, Industry Verticals and Others.

This helps us to gather the data related to players revenue, operating cycle and expense, profit along with product or service growth etc.

Almost 70-80% of data is collected through primary medium and further validation is done through various secondary sources that includes Regulators, World Bank, Association, Company Website, SEC filings, OTC BB, USPTO, EPO, Annual reports, press releases etc.

Report Objectives / Segmentation Covered

By Type

- Simple electronic signature (SES)

- Advanced electronic signature (AES)

- Qualified electronic signature (QES)

By Industry Vertical

- BFSI

- Government & Defence

- Real Estate

- Healthcare & Life Sciences

- Education

- Legal

- Others

By Deployment

- On-Premises

- Cloud

By Organisation Size

- Small

- Medium

- Large

By Regions

- South America

- Brazil

- Argentina

- Rest of South America

- Asia Pacific

- China

- Japan

- India

- South Korea

- Taiwan

- Australia

- Rest of Asia-Pacific

- Europe

- Germany

- France

- Italy

- United Kingdom

- Netherlands

- Rest of Europe

- MEA

- Middle East

- Africa

- North America

- United States

- Canada

- Mexico

- 1. Market Overview

- 1.1. Introduction

- 1.2. Scope/Objective of the Study

- 1.2.1. Research Objective

- 2. Executive Summary

- 2.1. Introduction

- 3. Market Dynamics

- 3.1. Introduction

- 3.2. Market Drivers

- 3.2.1. Fast growth in investments in electronic documents by governments and enterprises

- 3.2.2. Upgrade in end-to-end customer experience

- 3.2.3. Enhanced security with a controlled and seamless workflow

- 3.2.4. Improved operational efficiency at lower OPEX

- 3.3. Market Challenges

- 3.3.1. Intensely entrenched traditional business practices

- 3.3.2. Cost of implementation and legality issues

- 3.4. Market Trends

- 3.4.1. The growing number of connected devices, including smartphones, tablets, and laptop

- 3.4.2. Increasing E-Commerce Market Boosting the Growth of eSignature

- 4. Market Factor Analysis

- 4.1. Porters Five Forces

- 4.2. Supply/Value Chain

- 4.3. PESTEL analysis

- 4.4. Market Entropy

- 4.5. Patent/Trademark Analysis

- 5. Global eSignature and Certifications, by Type, Industry Vertical, Deployment, Organisation Size and Region (value) (2016-2021)

- 5.1. Introduction

- 5.2. Global eSignature and Certifications (Value)

- 5.2.1. Global eSignature and Certifications by: Type (Value)

- 5.2.1.1. Simple electronic signature (SES)

- 5.2.1.2. Advanced electronic signature (AES)

- 5.2.1.3. Qualified electronic signature (QES)

- 5.2.2. Global eSignature and Certifications by: Industry Vertical (Value)

- 5.2.2.1. BFSI

- 5.2.2.2. Government & Defence

- 5.2.2.3. Real Estate

- 5.2.2.4. Healthcare & Life Sciences

- 5.2.2.5. Education

- 5.2.2.6. Legal

- 5.2.2.7. Others

- 5.2.3. Global eSignature and Certifications by: Deployment (Value)

- 5.2.3.1. On-Premises

- 5.2.3.2. Cloud

- 5.2.4. Global eSignature and Certifications by: Organisation Size (Value)

- 5.2.4.1. Small

- 5.2.4.2. Medium

- 5.2.4.3. Large

- 5.2.5. Global eSignature and Certifications Region

- 5.2.5.1. South America

- 5.2.5.1.1. Brazil

- 5.2.5.1.2. Argentina

- 5.2.5.1.3. Rest of South America

- 5.2.5.2. Asia Pacific

- 5.2.5.2.1. China

- 5.2.5.2.2. Japan

- 5.2.5.2.3. India

- 5.2.5.2.4. South Korea

- 5.2.5.2.5. Taiwan

- 5.2.5.2.6. Australia

- 5.2.5.2.7. Rest of Asia-Pacific

- 5.2.5.3. Europe

- 5.2.5.3.1. Germany

- 5.2.5.3.2. France

- 5.2.5.3.3. Italy

- 5.2.5.3.4. United Kingdom

- 5.2.5.3.5. Netherlands

- 5.2.5.3.6. Rest of Europe

- 5.2.5.4. MEA

- 5.2.5.4.1. Middle East

- 5.2.5.4.2. Africa

- 5.2.5.5. North America

- 5.2.5.5.1. United States

- 5.2.5.5.2. Canada

- 5.2.5.5.3. Mexico

- 5.2.5.1. South America

- 5.2.1. Global eSignature and Certifications by: Type (Value)

- 6. eSignature and Certifications: Manufacturers/Players Analysis

- 6.1. Competitive Landscape

- 6.1.1. Market Share Analysis

- 6.1.1.1. Top 3

- 6.1.1.2. Top 5

- 6.1.1. Market Share Analysis

- 6.2. Peer Group Analysis (2021)

- 6.3. BCG Matrix

- 6.4. Company Profile

- 6.4.1. SignNow (United States)

- 6.4.1.1. Business Overview

- 6.4.1.2. Products/Services Offerings

- 6.4.1.3. Financial Analysis

- 6.4.1.4. SWOT Analysis

- 6.4.2. Aspose Pty Ltd (Australia)

- 6.4.2.1. Business Overview

- 6.4.2.2. Products/Services Offerings

- 6.4.2.3. Financial Analysis

- 6.4.2.4. SWOT Analysis

- 6.4.3. ContractSafe (United States)

- 6.4.3.1. Business Overview

- 6.4.3.2. Products/Services Offerings

- 6.4.3.3. Financial Analysis

- 6.4.3.4. SWOT Analysis

- 6.4.4. DocuSign (United States)

- 6.4.4.1. Business Overview

- 6.4.4.2. Products/Services Offerings

- 6.4.4.3. Financial Analysis

- 6.4.4.4. SWOT Analysis

- 6.4.5. Foxit Software Incorporated (United States)

- 6.4.5.1. Business Overview

- 6.4.5.2. Products/Services Offerings

- 6.4.5.3. Financial Analysis

- 6.4.5.4. SWOT Analysis

- 6.4.6. MSB (Sweden)

- 6.4.6.1. Business Overview

- 6.4.6.2. Products/Services Offerings

- 6.4.6.3. Financial Analysis

- 6.4.6.4. SWOT Analysis

- 6.4.7. Odoo (United States)

- 6.4.7.1. Business Overview

- 6.4.7.2. Products/Services Offerings

- 6.4.7.3. Financial Analysis

- 6.4.7.4. SWOT Analysis

- 6.4.8. OneSpan Sign (United States)

- 6.4.8.1. Business Overview

- 6.4.8.2. Products/Services Offerings

- 6.4.8.3. Financial Analysis

- 6.4.8.4. SWOT Analysis

- 6.4.9. Skribble (Switzerland)

- 6.4.9.1. Business Overview

- 6.4.9.2. Products/Services Offerings

- 6.4.9.3. Financial Analysis

- 6.4.9.4. SWOT Analysis

- 6.4.10. LULU Software Limited (Canada)

- 6.4.10.1. Business Overview

- 6.4.10.2. Products/Services Offerings

- 6.4.10.3. Financial Analysis

- 6.4.10.4. SWOT Analysis

- 6.4.11. Zoho Sign (India)

- 6.4.11.1. Business Overview

- 6.4.11.2. Products/Services Offerings

- 6.4.11.3. Financial Analysis

- 6.4.11.4. SWOT Analysis

- 6.4.12. Rpost (United States)

- 6.4.12.1. Business Overview

- 6.4.12.2. Products/Services Offerings

- 6.4.12.3. Financial Analysis

- 6.4.12.4. SWOT Analysis

- 6.4.1. SignNow (United States)

- 6.1. Competitive Landscape

- 7. Global eSignature and Certifications Sale, by Type, Industry Vertical, Deployment, Organisation Size and Region (value) (2022-2027)

- 7.1. Introduction

- 7.2. Global eSignature and Certifications (Value)

- 7.2.1. Global eSignature and Certifications by: Type (Value)

- 7.2.1.1. Simple electronic signature (SES)

- 7.2.1.2. Advanced electronic signature (AES)

- 7.2.1.3. Qualified electronic signature (QES)

- 7.2.2. Global eSignature and Certifications by: Industry Vertical (Value)

- 7.2.2.1. BFSI

- 7.2.2.2. Government & Defence

- 7.2.2.3. Real Estate

- 7.2.2.4. Healthcare & Life Sciences

- 7.2.2.5. Education

- 7.2.2.6. Legal

- 7.2.2.7. Others

- 7.2.3. Global eSignature and Certifications by: Deployment (Value)

- 7.2.3.1. On-Premises

- 7.2.3.2. Cloud

- 7.2.4. Global eSignature and Certifications by: Organisation Size (Value)

- 7.2.4.1. Small

- 7.2.4.2. Medium

- 7.2.4.3. Large

- 7.2.5. Global eSignature and Certifications Region

- 7.2.5.1. South America

- 7.2.5.1.1. Brazil

- 7.2.5.1.2. Argentina

- 7.2.5.1.3. Rest of South America

- 7.2.5.2. Asia Pacific

- 7.2.5.2.1. China

- 7.2.5.2.2. Japan

- 7.2.5.2.3. India

- 7.2.5.2.4. South Korea

- 7.2.5.2.5. Taiwan

- 7.2.5.2.6. Australia

- 7.2.5.2.7. Rest of Asia-Pacific

- 7.2.5.3. Europe

- 7.2.5.3.1. Germany

- 7.2.5.3.2. France

- 7.2.5.3.3. Italy

- 7.2.5.3.4. United Kingdom

- 7.2.5.3.5. Netherlands

- 7.2.5.3.6. Rest of Europe

- 7.2.5.4. MEA

- 7.2.5.4.1. Middle East

- 7.2.5.4.2. Africa

- 7.2.5.5. North America

- 7.2.5.5.1. United States

- 7.2.5.5.2. Canada

- 7.2.5.5.3. Mexico

- 7.2.5.1. South America

- 7.2.1. Global eSignature and Certifications by: Type (Value)

- 8. Appendix

- 8.1. Acronyms

- 9. Methodology and Data Source

- 9.1. Methodology/Research Approach

- 9.1.1. Research Programs/Design

- 9.1.2. Market Size Estimation

- 9.1.3. Market Breakdown and Data Triangulation

- 9.2. Data Source

- 9.2.1. Secondary Sources

- 9.2.2. Primary Sources

- 9.3. Disclaimer

- 9.1. Methodology/Research Approach

List of Tables

- Table 1. eSignature and Certifications: by Type(USD Million)

- Table 2. eSignature and Certifications Simple electronic signature (SES) , by Region USD Million (2016-2021)

- Table 3. eSignature and Certifications Advanced electronic signature (AES) , by Region USD Million (2016-2021)

- Table 4. eSignature and Certifications Qualified electronic signature (QES) , by Region USD Million (2016-2021)

- Table 5. eSignature and Certifications: by Industry Vertical(USD Million)

- Table 6. eSignature and Certifications BFSI , by Region USD Million (2016-2021)

- Table 7. eSignature and Certifications Government & Defence , by Region USD Million (2016-2021)

- Table 8. eSignature and Certifications Real Estate , by Region USD Million (2016-2021)

- Table 9. eSignature and Certifications Healthcare & Life Sciences , by Region USD Million (2016-2021)

- Table 10. eSignature and Certifications Education , by Region USD Million (2016-2021)

- Table 11. eSignature and Certifications Legal , by Region USD Million (2016-2021)

- Table 12. eSignature and Certifications Others , by Region USD Million (2016-2021)

- Table 13. eSignature and Certifications: by Deployment(USD Million)

- Table 14. eSignature and Certifications On-Premises , by Region USD Million (2016-2021)

- Table 15. eSignature and Certifications Cloud , by Region USD Million (2016-2021)

- Table 16. eSignature and Certifications: by Organisation Size(USD Million)

- Table 17. eSignature and Certifications Small , by Region USD Million (2016-2021)

- Table 18. eSignature and Certifications Medium , by Region USD Million (2016-2021)

- Table 19. eSignature and Certifications Large , by Region USD Million (2016-2021)

- Table 20. South America eSignature and Certifications, by Country USD Million (2016-2021)

- Table 21. South America eSignature and Certifications, by Type USD Million (2016-2021)

- Table 22. South America eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 23. South America eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 24. South America eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 25. Brazil eSignature and Certifications, by Type USD Million (2016-2021)

- Table 26. Brazil eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 27. Brazil eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 28. Brazil eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 29. Argentina eSignature and Certifications, by Type USD Million (2016-2021)

- Table 30. Argentina eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 31. Argentina eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 32. Argentina eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 33. Rest of South America eSignature and Certifications, by Type USD Million (2016-2021)

- Table 34. Rest of South America eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 35. Rest of South America eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 36. Rest of South America eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 37. Asia Pacific eSignature and Certifications, by Country USD Million (2016-2021)

- Table 38. Asia Pacific eSignature and Certifications, by Type USD Million (2016-2021)

- Table 39. Asia Pacific eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 40. Asia Pacific eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 41. Asia Pacific eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 42. China eSignature and Certifications, by Type USD Million (2016-2021)

- Table 43. China eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 44. China eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 45. China eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 46. Japan eSignature and Certifications, by Type USD Million (2016-2021)

- Table 47. Japan eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 48. Japan eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 49. Japan eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 50. India eSignature and Certifications, by Type USD Million (2016-2021)

- Table 51. India eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 52. India eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 53. India eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 54. South Korea eSignature and Certifications, by Type USD Million (2016-2021)

- Table 55. South Korea eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 56. South Korea eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 57. South Korea eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 58. Taiwan eSignature and Certifications, by Type USD Million (2016-2021)

- Table 59. Taiwan eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 60. Taiwan eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 61. Taiwan eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 62. Australia eSignature and Certifications, by Type USD Million (2016-2021)

- Table 63. Australia eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 64. Australia eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 65. Australia eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 66. Rest of Asia-Pacific eSignature and Certifications, by Type USD Million (2016-2021)

- Table 67. Rest of Asia-Pacific eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 68. Rest of Asia-Pacific eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 69. Rest of Asia-Pacific eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 70. Europe eSignature and Certifications, by Country USD Million (2016-2021)

- Table 71. Europe eSignature and Certifications, by Type USD Million (2016-2021)

- Table 72. Europe eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 73. Europe eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 74. Europe eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 75. Germany eSignature and Certifications, by Type USD Million (2016-2021)

- Table 76. Germany eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 77. Germany eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 78. Germany eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 79. France eSignature and Certifications, by Type USD Million (2016-2021)

- Table 80. France eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 81. France eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 82. France eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 83. Italy eSignature and Certifications, by Type USD Million (2016-2021)

- Table 84. Italy eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 85. Italy eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 86. Italy eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 87. United Kingdom eSignature and Certifications, by Type USD Million (2016-2021)

- Table 88. United Kingdom eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 89. United Kingdom eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 90. United Kingdom eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 91. Netherlands eSignature and Certifications, by Type USD Million (2016-2021)

- Table 92. Netherlands eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 93. Netherlands eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 94. Netherlands eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 95. Rest of Europe eSignature and Certifications, by Type USD Million (2016-2021)

- Table 96. Rest of Europe eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 97. Rest of Europe eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 98. Rest of Europe eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 99. MEA eSignature and Certifications, by Country USD Million (2016-2021)

- Table 100. MEA eSignature and Certifications, by Type USD Million (2016-2021)

- Table 101. MEA eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 102. MEA eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 103. MEA eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 104. Middle East eSignature and Certifications, by Type USD Million (2016-2021)

- Table 105. Middle East eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 106. Middle East eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 107. Middle East eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 108. Africa eSignature and Certifications, by Type USD Million (2016-2021)

- Table 109. Africa eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 110. Africa eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 111. Africa eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 112. North America eSignature and Certifications, by Country USD Million (2016-2021)

- Table 113. North America eSignature and Certifications, by Type USD Million (2016-2021)

- Table 114. North America eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 115. North America eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 116. North America eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 117. United States eSignature and Certifications, by Type USD Million (2016-2021)

- Table 118. United States eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 119. United States eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 120. United States eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 121. Canada eSignature and Certifications, by Type USD Million (2016-2021)

- Table 122. Canada eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 123. Canada eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 124. Canada eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 125. Mexico eSignature and Certifications, by Type USD Million (2016-2021)

- Table 126. Mexico eSignature and Certifications, by Industry Vertical USD Million (2016-2021)

- Table 127. Mexico eSignature and Certifications, by Deployment USD Million (2016-2021)

- Table 128. Mexico eSignature and Certifications, by Organisation Size USD Million (2016-2021)

- Table 129. Company Basic Information, Sales Area and Its Competitors

- Table 130. Company Basic Information, Sales Area and Its Competitors

- Table 131. Company Basic Information, Sales Area and Its Competitors

- Table 132. Company Basic Information, Sales Area and Its Competitors

- Table 133. Company Basic Information, Sales Area and Its Competitors

- Table 134. Company Basic Information, Sales Area and Its Competitors

- Table 135. Company Basic Information, Sales Area and Its Competitors

- Table 136. Company Basic Information, Sales Area and Its Competitors

- Table 137. Company Basic Information, Sales Area and Its Competitors

- Table 138. Company Basic Information, Sales Area and Its Competitors

- Table 139. Company Basic Information, Sales Area and Its Competitors

- Table 140. Company Basic Information, Sales Area and Its Competitors

- Table 141. eSignature and Certifications: by Type(USD Million)

- Table 142. eSignature and Certifications Simple electronic signature (SES) , by Region USD Million (2022-2027)

- Table 143. eSignature and Certifications Advanced electronic signature (AES) , by Region USD Million (2022-2027)

- Table 144. eSignature and Certifications Qualified electronic signature (QES) , by Region USD Million (2022-2027)

- Table 145. eSignature and Certifications: by Industry Vertical(USD Million)

- Table 146. eSignature and Certifications BFSI , by Region USD Million (2022-2027)

- Table 147. eSignature and Certifications Government & Defence , by Region USD Million (2022-2027)

- Table 148. eSignature and Certifications Real Estate , by Region USD Million (2022-2027)

- Table 149. eSignature and Certifications Healthcare & Life Sciences , by Region USD Million (2022-2027)

- Table 150. eSignature and Certifications Education , by Region USD Million (2022-2027)

- Table 151. eSignature and Certifications Legal , by Region USD Million (2022-2027)

- Table 152. eSignature and Certifications Others , by Region USD Million (2022-2027)

- Table 153. eSignature and Certifications: by Deployment(USD Million)

- Table 154. eSignature and Certifications On-Premises , by Region USD Million (2022-2027)

- Table 155. eSignature and Certifications Cloud , by Region USD Million (2022-2027)

- Table 156. eSignature and Certifications: by Organisation Size(USD Million)

- Table 157. eSignature and Certifications Small , by Region USD Million (2022-2027)

- Table 158. eSignature and Certifications Medium , by Region USD Million (2022-2027)

- Table 159. eSignature and Certifications Large , by Region USD Million (2022-2027)

- Table 160. South America eSignature and Certifications, by Country USD Million (2022-2027)

- Table 161. South America eSignature and Certifications, by Type USD Million (2022-2027)

- Table 162. South America eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 163. South America eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 164. South America eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 165. Brazil eSignature and Certifications, by Type USD Million (2022-2027)

- Table 166. Brazil eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 167. Brazil eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 168. Brazil eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 169. Argentina eSignature and Certifications, by Type USD Million (2022-2027)

- Table 170. Argentina eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 171. Argentina eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 172. Argentina eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 173. Rest of South America eSignature and Certifications, by Type USD Million (2022-2027)

- Table 174. Rest of South America eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 175. Rest of South America eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 176. Rest of South America eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 177. Asia Pacific eSignature and Certifications, by Country USD Million (2022-2027)

- Table 178. Asia Pacific eSignature and Certifications, by Type USD Million (2022-2027)

- Table 179. Asia Pacific eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 180. Asia Pacific eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 181. Asia Pacific eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 182. China eSignature and Certifications, by Type USD Million (2022-2027)

- Table 183. China eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 184. China eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 185. China eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 186. Japan eSignature and Certifications, by Type USD Million (2022-2027)

- Table 187. Japan eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 188. Japan eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 189. Japan eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 190. India eSignature and Certifications, by Type USD Million (2022-2027)

- Table 191. India eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 192. India eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 193. India eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 194. South Korea eSignature and Certifications, by Type USD Million (2022-2027)

- Table 195. South Korea eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 196. South Korea eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 197. South Korea eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 198. Taiwan eSignature and Certifications, by Type USD Million (2022-2027)

- Table 199. Taiwan eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 200. Taiwan eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 201. Taiwan eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 202. Australia eSignature and Certifications, by Type USD Million (2022-2027)

- Table 203. Australia eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 204. Australia eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 205. Australia eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 206. Rest of Asia-Pacific eSignature and Certifications, by Type USD Million (2022-2027)

- Table 207. Rest of Asia-Pacific eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 208. Rest of Asia-Pacific eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 209. Rest of Asia-Pacific eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 210. Europe eSignature and Certifications, by Country USD Million (2022-2027)

- Table 211. Europe eSignature and Certifications, by Type USD Million (2022-2027)

- Table 212. Europe eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 213. Europe eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 214. Europe eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 215. Germany eSignature and Certifications, by Type USD Million (2022-2027)

- Table 216. Germany eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 217. Germany eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 218. Germany eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 219. France eSignature and Certifications, by Type USD Million (2022-2027)

- Table 220. France eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 221. France eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 222. France eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 223. Italy eSignature and Certifications, by Type USD Million (2022-2027)

- Table 224. Italy eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 225. Italy eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 226. Italy eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 227. United Kingdom eSignature and Certifications, by Type USD Million (2022-2027)

- Table 228. United Kingdom eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 229. United Kingdom eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 230. United Kingdom eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 231. Netherlands eSignature and Certifications, by Type USD Million (2022-2027)

- Table 232. Netherlands eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 233. Netherlands eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 234. Netherlands eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 235. Rest of Europe eSignature and Certifications, by Type USD Million (2022-2027)

- Table 236. Rest of Europe eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 237. Rest of Europe eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 238. Rest of Europe eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 239. MEA eSignature and Certifications, by Country USD Million (2022-2027)

- Table 240. MEA eSignature and Certifications, by Type USD Million (2022-2027)

- Table 241. MEA eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 242. MEA eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 243. MEA eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 244. Middle East eSignature and Certifications, by Type USD Million (2022-2027)

- Table 245. Middle East eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 246. Middle East eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 247. Middle East eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 248. Africa eSignature and Certifications, by Type USD Million (2022-2027)

- Table 249. Africa eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 250. Africa eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 251. Africa eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 252. North America eSignature and Certifications, by Country USD Million (2022-2027)

- Table 253. North America eSignature and Certifications, by Type USD Million (2022-2027)

- Table 254. North America eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 255. North America eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 256. North America eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 257. United States eSignature and Certifications, by Type USD Million (2022-2027)

- Table 258. United States eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 259. United States eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 260. United States eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 261. Canada eSignature and Certifications, by Type USD Million (2022-2027)

- Table 262. Canada eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 263. Canada eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 264. Canada eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 265. Mexico eSignature and Certifications, by Type USD Million (2022-2027)

- Table 266. Mexico eSignature and Certifications, by Industry Vertical USD Million (2022-2027)

- Table 267. Mexico eSignature and Certifications, by Deployment USD Million (2022-2027)

- Table 268. Mexico eSignature and Certifications, by Organisation Size USD Million (2022-2027)

- Table 269. Research Programs/Design for This Report

- Table 270. Key Data Information from Secondary Sources

- Table 271. Key Data Information from Primary Sources

List of Figures

- Figure 1. Porters Five Forces

- Figure 2. Supply/Value Chain

- Figure 3. PESTEL analysis

- Figure 4. Global eSignature and Certifications: by Type USD Million (2016-2021)

- Figure 5. Global eSignature and Certifications: by Industry Vertical USD Million (2016-2021)

- Figure 6. Global eSignature and Certifications: by Deployment USD Million (2016-2021)

- Figure 7. Global eSignature and Certifications: by Organisation Size USD Million (2016-2021)

- Figure 8. South America eSignature and Certifications Share (%), by Country

- Figure 9. Asia Pacific eSignature and Certifications Share (%), by Country

- Figure 10. Europe eSignature and Certifications Share (%), by Country

- Figure 11. MEA eSignature and Certifications Share (%), by Country

- Figure 12. North America eSignature and Certifications Share (%), by Country

- Figure 13. Global eSignature and Certifications share by Players 2021 (%)

- Figure 14. Global eSignature and Certifications share by Players (Top 3) 2021(%)

- Figure 15. Global eSignature and Certifications share by Players (Top 5) 2021(%)

- Figure 16. BCG Matrix for key Companies

- Figure 17. SignNow (United States) Revenue, Net Income and Gross profit

- Figure 18. SignNow (United States) Revenue: by Geography 2021

- Figure 19. Aspose Pty Ltd (Australia) Revenue, Net Income and Gross profit

- Figure 20. Aspose Pty Ltd (Australia) Revenue: by Geography 2021

- Figure 21. ContractSafe (United States) Revenue, Net Income and Gross profit

- Figure 22. ContractSafe (United States) Revenue: by Geography 2021

- Figure 23. DocuSign (United States) Revenue, Net Income and Gross profit

- Figure 24. DocuSign (United States) Revenue: by Geography 2021

- Figure 25. Foxit Software Incorporated (United States) Revenue, Net Income and Gross profit

- Figure 26. Foxit Software Incorporated (United States) Revenue: by Geography 2021

- Figure 27. MSB (Sweden) Revenue, Net Income and Gross profit

- Figure 28. MSB (Sweden) Revenue: by Geography 2021

- Figure 29. Odoo (United States) Revenue, Net Income and Gross profit

- Figure 30. Odoo (United States) Revenue: by Geography 2021

- Figure 31. OneSpan Sign (United States) Revenue, Net Income and Gross profit

- Figure 32. OneSpan Sign (United States) Revenue: by Geography 2021

- Figure 33. Skribble (Switzerland) Revenue, Net Income and Gross profit

- Figure 34. Skribble (Switzerland) Revenue: by Geography 2021

- Figure 35. LULU Software Limited (Canada) Revenue, Net Income and Gross profit

- Figure 36. LULU Software Limited (Canada) Revenue: by Geography 2021

- Figure 37. Zoho Sign (India) Revenue, Net Income and Gross profit

- Figure 38. Zoho Sign (India) Revenue: by Geography 2021

- Figure 39. Rpost (United States) Revenue, Net Income and Gross profit

- Figure 40. Rpost (United States) Revenue: by Geography 2021

- Figure 41. Global eSignature and Certifications: by Type USD Million (2022-2027)

- Figure 42. Global eSignature and Certifications: by Industry Vertical USD Million (2022-2027)

- Figure 43. Global eSignature and Certifications: by Deployment USD Million (2022-2027)

- Figure 44. Global eSignature and Certifications: by Organisation Size USD Million (2022-2027)

- Figure 45. South America eSignature and Certifications Share (%), by Country

- Figure 46. Asia Pacific eSignature and Certifications Share (%), by Country

- Figure 47. Europe eSignature and Certifications Share (%), by Country

- Figure 48. MEA eSignature and Certifications Share (%), by Country

- Figure 49. North America eSignature and Certifications Share (%), by Country

List of companies from research coverage that are profiled in the study

- SignNow (United States)

- Aspose Pty Ltd (Australia)

- ContractSafe (United States)

- DocuSign (United States)

- Foxit Software Incorporated (United States)

- MSB (Sweden)

- Odoo (United States)

- OneSpan Sign (United States)

- Skribble (Switzerland)

- LULU Software Limited (Canada)

- Zoho Sign (India)

- Rpost (United States)

Select User Access Type

Key Highlights of Report

Sep 2022

214 Pages

67 Tables

Base Year: 2021

Coverage: 15+ Companies; 18 Countries

Request Sample Pages

Budget constraints? Get in touch with us for special pricing

Check Discount Now

Talk to Our Experts

Want to Customize Study?

"We employ Market statistics, Industry benchmarking, Patent analysis, and Technological Insights to derive requirements and provide customize scope of work."

Frequently Asked Questions (FAQ):

Top performing companies in the Global eSignature and Certifications market are SignNow (United States), Aspose Pty Ltd (Australia), ContractSafe (United States), DocuSign (United States), Foxit Software Incorporated (United States), MSB (Sweden), Odoo (United States), OneSpan Sign (United States), Skribble (Switzerland), LULU Software Limited (Canada), Zoho Sign (India) and Rpost (United States), to name a few.

"The growing number of connected devices, including smartphones, tablets, and laptop

" is seen as one of major influencing trends for eSignature and Certifications Market during projected period 2021-2027.

Simple electronic signature (SES)

segment in Global market to hold robust market share owing to "Fast growth in investments in electronic documents by governments and enterprises

".